![]() You don't need to be an 'investor' to invest in Singletrack: 6 days left: 95% of target - Find out more

You don't need to be an 'investor' to invest in Singletrack: 6 days left: 95% of target - Find out more

Via her part-time job, Jnr has managed to accumulate some £'s.

She is contemplating buying Premium Bonds for a no-risk, potential return.

Pros and cons of Premium Bonds?

Spoke to some folks at work and a few have managed to get a decent return via prize wins.

No experience myself, but I do remember a monster thread on here that's been running for some time, presumably there'll be some info. in there.

https://singletrackmag.com/forum/topic/its-premium-bonds-draw-day/

Personally having held PB's for 20 odd years, unless you've maxed out an ISA and other saving accounts then i' d use them first. At one time I had around £10k in and was winning maybe £100 a year, currently my cash ISA would give me way more, even if the chance of a big win is no longer there.

Thing to remember is that if you win nothing repeatedly then inflation is decreasing the value of your savings.

You may "win" you may not. It's a gamble, I had a few £000 in and "won" £50. Took it out and stuck it in an ISA which is returned 10% this yr

For a more certain return jnr savings account

I've got a few grand in for emergency funds, it's easy access and gives a mild thrill when you get 'the email'. I have won a few quid but I've basically had average luck, 25 here, 50 there.

If my Isa allowance was maxed out each year then I might start buying more. But it isn't so I dont

But really, I would be sitting up an Isa for them and just drip drip money into that on a direct debit. If you start early you will save a fortune and won't really notice it going out, and get into the habit of saving

Otherwise before you know it you're mid 50s and thinking I hate my job, if only I had some decent savings I could quit and do something else

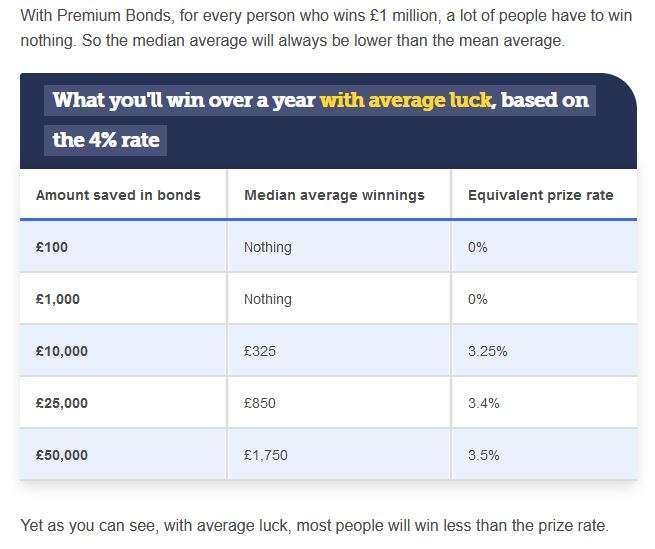

The average return on premium bonds has dropped to below 4% for a full holding of 50K, if you have 'average luck' - the odds drop if you have a lower holding, and really fall off a cliff for smaller amounts.

As above, fill up thier ISA allowance first, even just a cash ISA, decent ones are paying around 5%, and it's tax free guaranteed return.

https://www.moneysavingexpert.com/savings/best-cash-isa/

Beats premium bonds like a ginger step child all day long - yes you could win a million quid but the odds are crazy.

Best way to think of premium bonds is to think of it as a lottery, but you get to re-play your stake every month.

EDIT,

For example, I've had 50K in PB for 4 draws now, ...if I extrapolate my total winnings to 12 months I'm running at 3.4% return on investment, so not very clever really considering my instant access savings is 4.35% and my cash ISA is 4.9%.

£5k and I never win anything beyond maybe £25-£50 per year.

Stick it in an ISA or buy some gold*

*Think I heard recently that gold prices could possibly rise substantially in the near future.

I calculated last year how much interest would have been earned on the £50k in my premium bonds account and it worked out almost the same amount, a little bit less. However, I dont decide where the 'pot' lives and until it's mine it's staying where it is.

Bucking the trend I won slightly more than the expected return last year, so much better than an ISA for me. And a very small chance of doing a lot better.

I'm stoozing some credit cards so I'm not playing with my own money so technically my return on investment is infinity as a percentage

Bucking the trend I won slightly more than the expected return last year, so much better than an ISA for me. And a very small chance of doing a lot better.

But you got lucky... statistically speaking you'll make a lot less over time than a cash ISA.

The kids maxed out on their inheritance from MrsMC's parents, 4% probably about right.

I've got a few '000 which came from my Nan. Probably get £500-£1000 a year (would have to check, but win*something* most months). Every time I think of shifting to an ISA it's like cancelling my long term lottery ticket. I *might* win big next month...

I’ve got a few ‘000 which came from my Nan. Probably get £500-£1000

Those figures are pretty meaningless unless you tot up your winnings over 12 months and compare the winnings to the amount of premium bonds you hold, as a percentage.

And then compare that to what you'd get if it was in a cash ISA, for example.

You can see all your historical winnings on the NS&I website to calculate it quickly.

For example I've had 40k in a cash ISA for almost 12 months, earning about £5.44 interest per day at the moment (compound interest works both ways!) - so almost 2 grand a year in tax free interest... and that's money in the bank, every month, no luck involved.

I also hold 50k in premium bonds, but I'll be dumping 20k of that into an S&S ISA come April.

But you got lucky… statistically speaking you’ll make a lot less over time than a cash ISA.

Definitely. But sometimes people do get lucky. Whether I'll get lucky again this year who knows (I won nothing in January so that's not a great start...) I'm not expecting to but it's possible

Whether I’ll get lucky again this year who knows (I won nothing in January so that’s not a great start…) I’m not expecting to but it’s possible

Head to Vegas and play some BlackJack if you feel lucky, lol!

Pb s only really work if you are maxed out on isa s and a higher rate tax payer. I m averaging 4% on a maxed out holding, not bad but not brilliant.

Does it not depend what she wants to do with the money?

Got to be pension if saving for old age. Money in now will make a big difference come retirement.

ISA or LISA if saving for a house or is likely to need the money at a younger age.

I've got £10k in Premium Bonds and have only won a couple of hundred in the last year. My stocks and shares ISA is making a lot more than that.

+1 on just lock it in a savings account if you want some risk free and guaranteed returns.

My wife bought a fair 'chunk' with some inheritance. She's other small pots, but the 'chunk' has won regular this last two years, more than any bank interest. It does seem that your chances are higher with a number of bonds 'together'.

Typical stw....We are speaking about jnr with her pt job savings here, not those who have acquired wealth by death or yrs and yrs of savings.

PB are not the place for few £'s

Typical stw

I don't think anyone's recommended premium bonds over ISAs or pensions if they've not already used their ISA allowance?

Putting it into an ISA or increasing pension contributions are both decent ideas depending on the person's goals. Or maybe even a LISA if they are saving for a house but that comes it's own caviats.

Personally I dont use premium bonds. Unless you have 50k its very swingy in returns, and unless you get very lucky you'll get better average returns elsewhere.

I would stick it in the highest easy access saver you can, and DCA into a global index fund (e.g. VWRP), being ready for the buying opportunities that the next year will probably bring given the uncertainty the trump administration is causing the markets.

How quickly is she looking for a return, as my Nan won £25,000 last year, aged 103…