![]() You don't need to be an 'investor' to invest in Singletrack: 6 days left: 95% of target - Find out more

You don't need to be an 'investor' to invest in Singletrack: 6 days left: 95% of target - Find out more

Found out today that one of my daughters' girlfriends ( currently 21 ) has a debt of £12000 amassed over the period of about a year when she 19-20. The bank have given her a credit card and a bank overdraft and she has another credit-card for £3.5k....,lucrative, enticing online offer.

At the time she was earning £18k pa.

Now I know we can all utter " its her own fault " etc. but where's is the responsible lending on behalf of the bank? She's hardly paying anything off of her original debt just the interest.

Boils ma pi$$, I tell thee. Total disregard for a young persons life.

How many cases of depression or even suicide in young adults can be traced back to debt?

Any advice?

Can I take a guess at Natwest?

EDIT: Not wishing to make light of issue BTW, I completely agree with you.

advice for a 21 year old? go bankrupt! 😆

Can I take a guess at Natwest?

I'm going with [s]Natwest[/s] Ratsnest as well. They did similar to me when I was in business. They give you a brolly when It's sunny then want it back when it rains.

Interesting, I thought that sort of lending was a thing of the past. Tragic though, as you say. It could be a mill stone around her neck for years.

My current credit card with Santander has a pretty low credit limit (~1 month gross income). It's paid off in full every month and always has been for years and they won't increase it any more (I asked as I sometimes need it for business expenses).

Changed days from my first proper job when my bank without asking were offering £10k credit limits as soon as the account was opened!

My advice to her would be to get as much credit as she can possibly get from whoever is stupid enough to give it to her and have one hell of a party, or couple of years travelling, then go bankrupt.

barclays regularly offer me a pre-approved unsecured loan of ~£50k, money in my account by the end of the day.

so much for responsible lending...

The various credit card companies have no way of knowing about each other, so it's easy to build up multiple cards especially if you lie about having no other cards. £12k in debt is £120 a month in interest so that's affordable, but clearly unwise to have run up the debt. My 21 year old will owe £45k when she finishes Uni

Does [i]she[/i] think it's a problem? If not, there's nothing much you can do.

If she does then get her to get rid of her CCs. Then check out what interest rates she is paying and try to get something arranged at a lower rate. That will mean some sort of loan. She might need someone to act as guarantor - her parents perhaps?

my latest 0% credit card started with an £8k limit and will go up if i make regular payments, which i have to as its direct debit...

A buffoon I know declared bankruptcy in 05 at 27 owing 50K all cards and loans with zero to show for it. Unless you count BB guns and console games as worth while.

His best mate is an architect while he worked for a waste management company in customer service. It was all to keep up with his mate.

He then got married paid for with cards and loans, has 2 kids and is just about done paying off his debts now and I doubt he will ever get on the property ladder.

At that age it's entirely the customers fault. I remember myself at that age, me and my then girlfriend used to ring up our CC providers and ask for an extension to the limit and when they approved it we'd go straight down and withdraw it in cash and then go to the students union. I wince when I think what I was like, withdrawing cash from a credit card!!!! I just didn't care about the consequences. Ending going default on 3 ccs just as I entered the job market.

A buffoon I know declared bankruptcy at 27 owing 50K all cards and loans with zero to show for it. Unless you count BB guns and console games as worth while.

I bet he had a hell of a good time pissing it up against the wall though and didnt have the stress of being an architect.

Interesting, I thought that sort of lending was a thing of the past.

So did I, until I started needing some recently. You really would not believe the amount of unsecured borrowing I have access to, from a very modest income. You really wouldn't!

This is in place of HIL to do up house, so it's actually served me well with lots of 0% deals on purchases & balance transfers credit cards.

With age and experience I will not get carried away and use this to my advantage and within my means, but if I was 18?

EDIT: Sorry, just realised this doesn't answer your question OP, just empathising with the fact 'irresponsible' lending is easily believable, still.

He's not that type, I've edited since you posted.

just as irresponsible borrowing.

she should know better at 21.....a fully grown adult.

are her parents sharing your concerns?

she should know better at 21.....a fully grown adult.

..and let's not have any of this crap, eh?

@jamblaya - actually they do - credit files contain the details off all creditors, balances, limits and of course payment history. They're supposed to review these periodically.

It's also a requirement for the financial companies to complete a income and expenditure review at the start of any new credit agreement.

As for the OPs friend - bankruptcy is actually not a bad idea - she'd have no problem proving she cannot afford to repay her debts and have a normal lifestyle and the court will ask her to pay an affordable amount each month for a few years. Yes she'll be a 'bankrupt' for 5 years, but she's young and the only downside of being bankrupt is you can't borrow any money - but it sounds like that's for the best - plus no respecable bank will lend to her with that amount of debt and that income anyway, there's very few downsides.

Need to find out why she is spending the money she hasn't got or the problem will only get worse.

As others have said, her route out may be bankruptcy. It will be no bed of roses, but after 6 years and lots of work she will be debt free and no one will be any the wiser.

Of course that's the cowards way out as in many ways she's not in that much debt.

I used to work for Barclays and it was this irresponsible lending practice that made me quit. I even stated that in my resignation letter (although

I used the word immoral). That was back in 2008 and I thought the financial crisis would have stopped this conduct.

Sadly not. I've heard from former colleagues that it is now worse than it ever was! They will never learn (the banks).

As for how credit cards can balloon in the credit available, I have a credit card that I started with Lloyds back in 2001 as a basic £500 limit one for students. It now has a pre-approved limit of £45k. I recently cancelled my Barclaycard that had a limit of £28k and I still got letters offering an increase. That's over 3 year's wages available on plastic immediately! With that kind of spending power available it's far too easy for young people to succumb.

It's definitely one of those varying company things then. We have a tesco cc and put at least a grand on it each month which gets paid off each month. The limit is still at 5k after what must be three years of doing that.

You can of course contact your CC provider and ask for your limit to be reduced.

Which is responsible borrowing, as opposed to egoistic willie waving 😀

£12k in debt is £120 a month in interest so t

Surely that depends entirely on the interest rate 😕

Doesn't seem great frankly, but she'll learn!

The reason for the ever increasing credit limit is for the type of people who will spend on the card, pay off some of it, preferably the minimum payment, then next month spend some more, and so on.

If you pay it off in full and never incurr interest charges then you're the worst type of customer. They don't make any money from you.

On one of my CC that I use for business expenses, the credit limit has tripled in the last five years. That was because I'd put flights and hotel bills for a number of people on it, thousands in some cases, and then not paid it in full because I had not received it all back from the accounts department. (They did start paying promptly when I put the interest payment on the expenses as well).

I can see how it would be tempting to spend the easily offered credit, but there has to be some responsibility held by the OPs daughters friend. She did spend the money, she should pay it back. Going bankrupt is just putting that debt back onto all of the other banks customers. That's why people who save or take credit responsibly have to subsidise the bad debtors with low savings rates and high CC rates.

The bank or CC company are sure as hell aren't going to take the loss.

I just swapped CC to Tesco - expecting the £1500 limit of my old card.

They gave me immediate £10k, and after six months of using/paying off in full (I use it for work travel expenses each month), they just upped it to £15k without asking or requesting.

I also just looked into car loans etc, and could borrow a rather impressive amount over 5 years.

I do not have any other debts, other than two mortgages on two properties, but this does seem a return to the 'lend more, make more profit' days.

£1000 every month on top of her wages? I thought I was bad maxing out a £1200 card on clothes at that age, but at least I wasn't earning. That's pretty appalling.

It may be irresponsible by the bank. But she is 21 for goodness sake. She isn't some helpless victim.

The bad news is the UK personal debt situation is about to get a whole lot worse, believe it or not.

[img]  [/img]

[/img]

I was talking to a friend last week who works in the Bank of England and asking him what the underlying driver of this forecast is and he simply said 'increased access to credit'

Personally I'm wondering if we've all gone stark, raving mad 😯

Poor thing, spunking £30,000 up the wall in a year.

My.

Heart.

Bleeds.

[quote=wanmankylung ]My advice to her would be to get as much credit as she can possibly get from whoever is stupid enough to give it to her and [b]pretend to[/b] have one hell of a party, or couple of years travelling, [b]whilst hiding it all offshore [/b]then go bankrupt.

Well if you can't beat them you might as well join them 😈

she should know better at 21.....a fully grown adult.

..and let's not have any of this crap, eh?

You're kidding right? The STW collective are too righteous to let this transgression slip, hell, why not just about triple the figure to 30k for good measure in some good old chinese whispers action.

Never mind the fact that you self righteous pricks know nothing of the womans personal circumstances the OPs point still stands, it was irresponsible to lend that amount of money full stop. As for the whys of having that amount of debt, there are plenty of noble, if misguided, ways that folk (and in my experience, plenty of women) end up in these places so why not leave the moral outrage for something you know the full facts on for once eh?

No real help, but I'm wondering about the wider social aspect that says this sort of borrowing is OK.

Years ago, before I got a mortgage & was sharing a rented house with a friend I wasn't earning very much & was living hand to mouth through too much partying etc.

My friend said get a credit card, its normal, everyone does it & everyone has debt.

I did so & it started to spiral of course, got on top of it & got a mortgage etc. When I split up with my ex & was paying for the whole household costs again I made the decision to address the outstanding cc bill as it was worrying me - it was for £600 & giving me a bit of worry!

Maybe its me, but I HATE debt & only use cash/debit card nowadays, if I don't have the money I wait til I have & save up. It seems I'm in the minority.

The bad news is the UK personal debt situation is about to get a whole lot worse, believe it or not.

Who the hell cooks up a forecast graph like that? Low and dropping slightly straight into a massive rise? I reckon they sneezed when the pen was on the paper!

There are many situations where people genuinely get into cc debt paying bills, putting food on the table for the kids & paying the utility bill, but equally there are people who use them as a way to fund a desired lifestyle that they can't otherwise afford. And for these people I have very little sympathy when they get themselves into debt. It's just greed and burying their heads in the sand so they can have the latest car on the drive or an expensive hand bag draped over a shoulder.

We had a young contractor start at a place I worked at several years ago - lab technician, so not brilliantly paid, but not minimum wage either.

He boasted about how he already had £10k debt that his dad had paid off. He had a Punto that was costing him £330/month to insure as he wrote his last one off when he was 18. He used to go to London with mates straight after work on Friday night every week and stay in decent hotels until Monday morning, they'd eat out the whole time, go clubbing every night and he used to boast about only drinking champagne.

He was back up to £19k debt and was planning a few more blowout weekends before declaring himself bankrupt.

He knew exactly what he was doing, but just didn't care.

Amazed the banks kept lending him the money, but he was completely aware of the hole he was digging for himself and seemed quite proud of it.

Nice infographic. I believe everything it says now, although I would have more faith if it had some green in it, a more reliable color.

I called the bank re a new mortgage last week. After a 10 minute phone call, they were happy to lend me a ridiculous amount of money. Not that I want that much, was just curious.

Why can't we all learn ??

Phone companies are the same. Even when in arrears it seems that phone shops have the ability to override all the "computer says no" bits and give people additional new contracts. My sister isn't the brightest financially and whenever she wants a new phone, just starts a new contract. Every six months or so. Never hear of a rejection even with the list of final warnings piling up by the door.

Never mind the fact that you self righteous pricks know nothing of the womans personal circumstances the OPs point still stands, it was irresponsible to lend that amount of money full stop.

True I know nothing of this girl so i have to make assumptions. I doubt from the info given she's borrowed this money to keep food on the table for her family or to look after an elderly relative. My assumption is that she's pi$$ed it up the wall in bars and handbag shops.

when I met my wife she was in a similar (actually x3 worse) position. It was all her own fault. She thought she could have it all now without paying for it. In my wifes case I lay the blame squarely on her mother (not the banks) who sat and watched it happen and hadn't taught her the value of saving rather than borrowing to fund her desired lifestyle.

And I thought my £8k credit card was excessive and too much! £45k? You could buy a northern terrace for that!

I don't have a cc. If you can't afford it, don't have it. Debt equals stress and lining the pockets of the bankers.

Although I didn't have to, it was cheaper for me to borrow £5k to buy my current runaround. However, when on the phone to the bank - which is the bank I use for my direct debits & bills NOT my main account, the conversation went like this;

Bank: "So you can't demonstrate regular salary onto this account?

Me: No

Them: "Hmm, that means we couldn't offer you the loan <pause> Hold on though, you do may a regular one off payment INTO the account which is equivalent to the bills going OUT of the account?"

Me: "yes, thats right, by standing order"

Them: "So, for the purpose of this phone, if we pretend that the income was 'salary' I would be able to offer you the loan.

Me: "Erm, yes OK...."

Them: "Congrats, we are able to offer you the loan. Once you have responded to our secret password text, £5k will be deposited into this account within the hour"

And it was. I never even proved my salary or total outgoings, no wonder people get into debt.

Its absolutely bonkers! Have we learn nothing? It does seem that we, as a society, appear to be trying to exactly replicate the conditions to led to the last crash.

The fact of the matter is that there is no economic recovery worthy of the name. There has been no rebalancing of the economy. Quite the reverse. So we have a government cynically trying to give the impression that everything hunky dory again through crazy short term policies, which are absolutely guaranteed to go tits up. And opposition parties entirely complicit in this neoliberal facade, offering absolutely no alternatives

So what have we got? Again....

A ridiculous and unsustainable housing bubble fuelled by public money (the frankly insane Help to Buy scheme), and another huge splurge on Buy-to-Let mortgages? (up 26% in 12 months)

Check!

A surge in consumer spending, despite a fall in salaries and 'real' income, all fuelled by cheap credit, while rates remain (temporarily) low?

Check!

Banks still 'Too Big to Fail' lobbing money around in the same 'we can't lose' manner as pre 2007?

Check!

The return of still totally unregulated, snouts-in-the-trough, big bonus, roulette-wheel, casino banking.

Check!

What could possibly go wrong? 🙄

[quote=binners ]What could possibly go wrong?

Don't worry, the Tories are in charge now, and we all know they're much better at managing the economy than Labour, so won't make the same mess as Brown and Darling.

People have lost the art of delayed gratification.

They also like to blame others for their predicament instead of looking at the real reason (their lack of judgement and wanting everything on a plate today not tomorrow)

BillMC - Member

I don't have a cc. If you can't afford it, don't have it. Debt equals stress and lining the pockets of the bankers.

So everyone should rent and line the pockets of the landlord instead?

jekkyl - MemberSo everyone should rent and line the pockets of the landlord instead?

Did you buy your house with a CC?

binners - MemberWhat could possibly go wrong?

Europe (where all the money is suddenly coming from) could fail, Russia could destabilise the Baltic states, labour could get into office with a workable majority, the two former would see the dollar return as safe haven currency increase in value and the cost of energy rising, the latter will see sterling drop in value with a similar effect.

But as far as the banks go, there are the Basle agreements in place keeping their debt to cash ratio regularly stress tested, we have a degree of security here in the property market thanks to years of under supply and influx of population.

So short of ISIS getting their hands on chemical or nuclear weapons I think we'll just see another bubble for a period until one or other event crack down the finance shutters again, I like that idea up there of borrowing everything you can, hiding it offshore then declaring bankruptcy - nice idea..

Or play the banks at their own game. If you shop round you can get interest free credit cards with 24 months intro offers, and cashback deals on groceries and fuel. The same bank offers you higher interest on your current balance than most ISAs. So, use THEIR credit card for 24 months food and fuel, earning 3% in cashback on the fuel, 1% cashback on groceries, and 2% on department store spending, ensure you leave the equivalent in your current account, where it earns a further 2-3% interest. Make sure the balance of the card never exceeds the balance of the current account, and never exceeds the credit limit. Pay it all back after 24 months and trouser the interest AND cashback. Takes discipline, and you have to make a 1% min payment on your card, but basically it's free money. The sweetest bit is that you are borrowing their money for free, to earn their interest on cash which you wouldn't otherwise have had

Paying off a credit card debt? Transfer a current credit card balance onto a free balance transfer card, set up a direct debit to pay off the 1% minimum charge on your new 0% card. Divide the total debt into 12 monthly sums, and put those into an interest earning account each month, less the 1% minimum that you're paying off anyway. At the end of the interest free balance transfer period pay off the credit card with the savings. Quite a difference between earning a few percent interest on the accumulating balance and spaffing 20% AER on the old credit card debt.

DO NOT do either of these things if you can't spend within your means, or organize your accounts to make sure you don't miss any payments or balance clearance deadlines.

[img] [/img]

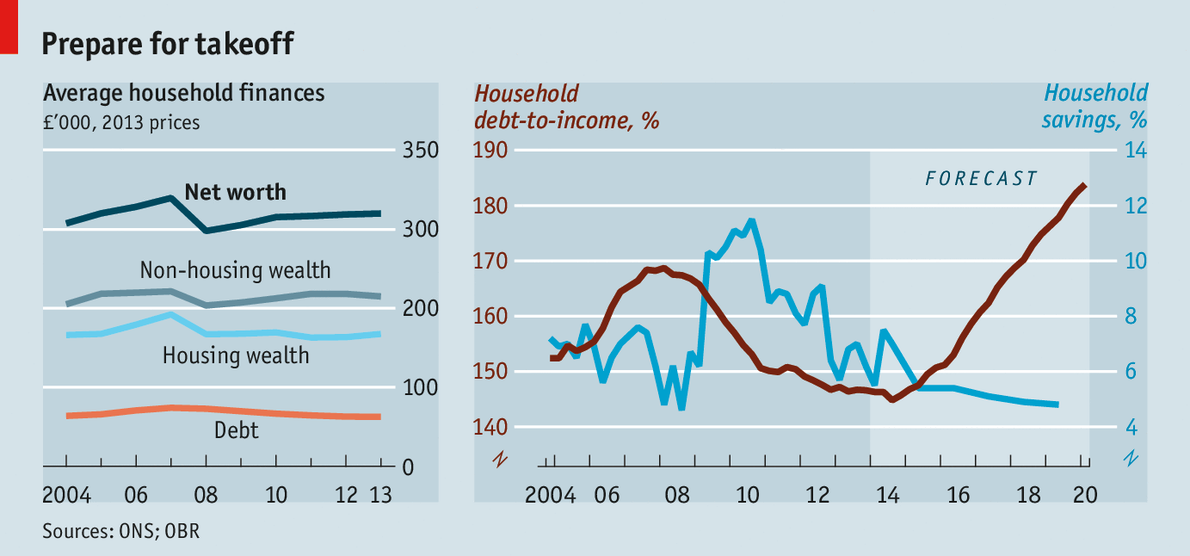

Average non-housing household wealth of £200,000?

I should coco!

Paying off a credit card debt? Transfer a current credit card balance onto a free balance transfer card, set up a direct debit to pay off the 1% minimum charge on your new 0% card. Divide the total debt into 12 monthly sums, and put those into an interest earning account each month, less the 1% minimum that you're paying off anyway. At the end of the interest free balance transfer period pay off the credit card with the savings.

If you ignore the 3.5% minimum balance charge that usually comes with the "deal". Know anywhere offering 3.5% savings barring a current account tied deal with minimum monthly deposit? Tarting isn't the payday it once was sadly. Low interest rates and inflation have knocked that well on the head.

True I know nothing of this girl so i have to make assumptions.

No actually, you don't, you only feel compelled to do for reasons best known to yourself.

I doubt from the info given she's borrowed this money to keep food on the table for her family or to look after an elderly relative. My assumption is that she's pi$$ed it up the wall in bars and handbag shops.

Really? Why's that? You don't think there's a possibility she could have been supporting a former partners indiscretions? It happens more than folk care to admit either through direct manipulation or from thinking they can help them. Abusive relationships aren't all physical, I've met enough people who have been in exactly this situation to know better than to make snarky throwaway remarks as you, and other here, do without understanding the whole situation.

Just because your wife spent beyond her means for the sake of a "better" lifestyle doesn't mean everyone who ends up with debt problems has.

[img] [/img]

Sure they haven't got "Debt" and "Non housing wealth" mixed up?

If you ignore the 3.5% minimum balance charge that usually comes with the "deal". Know anywhere offering 3.5% savings barring a current account tied deal with minimum monthly deposit? Tarting isn't the payday it once was sadly. Low interest rates and inflation have knocked that well on the head.

There are quite a few out there with sub 3% balance transfer charge, Nationwide, Fluid, Barclaycard, MBNA, Sainsbury..... and 0% intros are gradually expanding towards 34 months. So the savings earn extra and the repayments are spread further.

Barclaycard do on with 2% fee and 25 months 0%

And no, not many 3% interest earning accounts without monthly deposit. However, if you get a 34 month balance transfer on a card with 2.75 transfer fee, a 1.5%-2% savings account should do the trick. This example isn't a payday like stoozing can be, but it is a tidy saving on 20% debt.

Why would anyone, banks or overextended borrowers, hold back? They've learnt nothing as they've suffered no consequences.

The banks are stuffed with public money and the public are cheering the 'affordability' of more debt that comes from historically too low interest rates.

Humans only learn from bitter experience and since pretty much everyone was bailed out in 2008/9 the party has continued, and will until something properly goes pop.

I ended up with a £10k CC balance when I was in my early twneties.

Working away and my girlfriend used my CC on a bingo site and spent the £10k in 5 days. I threw up when I found out.

When I discussed it with the CC company (goldfish) they said that they didn't spot anything unusual!?! The bill was pages and pages of £50 payments to some online casino .com and they though it was fine!

We are no longer together...

Working away and my girlfriend used my CC on a bingo site and spent the £10k in 5 days. I threw up when I found out.

still together?

edit well there you go!.

[b]jimbobo[/b]

And I thought my £8k credit card was excessive and too much! £45k? You could buy a northern terrace for that!

I cancelled it this morning and paid off the £96 on it (used it for online purchases only). I now only have a Nationwide card with a £300 balance (0% for 6 months) and have reduced the limit from £2700 to £1000. That's £47.5k of potential credit gone, should improve my (pretty good TBH) credit score 😀

Now if we could have a housing crash (a proper one please) so that I can afford a reasonable house with a mortgage and a 10% deposit rather than the crummy flats I could get currently I'd be very happy 😈

[quote=milky1980 ] That's £47.5k of potential credit gone, should improve my (pretty good TBH) credit score I'm not sure it works like that. Having unused credit might show you as a responsible borrower?

Sort of, it'll show as only 1 card and one loan (car) totalling ~£3k rather than 3 cards and a loan totalling ~£3k with £47k of additional available pre-approved. Researched all this when I was working in the bank and my last mortgage advice meeting said it was still the same. Otherwise what would stop me getting a maxxed-out mortgage of £78k and then blowing the £45k C/C on house improvements/holidays/bikes to fill new shed?

Having a small C/C limit of £1k and never going near it and paying off regularly is the best. The absolute worst thing you can do (other than bankrupt) is have no credit history at all!

Yeah. Credit scores are a perverse thing.

A mate of mine had an absolute nightmare getting a mortgage! He'd always done that crazy old-fashioned thing of saving up for stuff, and only spending what he earned. So because he'd never had a credit card or personal loan, he had no credit rating. Nobody wanted to give him a mortgage, despite the fact he'd saved a massive deposit 😯

Two of my friends had the same problem, never had any credit. Not even a Contract mobile!

I suggested they should have a word with the CAB and that getting a small credit card to use for shopping and paying it off every bill might help. The CAB said the same thing so they both got a C/C and a contract mobile, lo and behold 12 months later they had a lovely big mortgage and at a low rate too.

Financially penalised (12 month's rent!) for doing the right thing whereas if you blow it all when you're young you get it thrown at you! Madness.

Having recently completed a study on Credit cards (I work for a regulator), I can honestly say I'd never ever have another credit card. Lending criteria, terms and conditions on said card, what happens if you miss a payment - no thanks. I'm sure some people are disciplined enough to make sure they clear it every month without fail, but for me personally if I can't afford it then I won't buy it and I certainly wouldn't put it on a CC.

At least the pay day lenders are up front...

[quote=flange ]Having recently completed a study on Credit cards (I work for a regulator), I can honestly say I'd never ever have another credit card. Lending criteria, terms and conditions on said card, what happens if you miss a payment - no thanks. I'm sure some people are disciplined enough to make sure they clear it every month without fail, but for me personally if I can't afford it then I won't buy it and I certainly wouldn't put it on a CC.

At least the pay day lenders are up front...

We pay everything on Tesco CC and pay it off each month. Then we get Tesco Clubcard points and I trade them in for Evans vouchers 🙂

We pay everything on Tesco CC and pay it off each month. Then we get Tesco Clubcard points and I trade them in for Evans vouchers

And to be fair, the affinity provider for the Tesco card probably hates you.

EDIT: To give some detail, because you're not the type of borrower they want. What they would prefer is that they tempt you in with an offer of 0% on purchases. When the term runs out, you've hopefully accumulated a 'balance' that needs to be cleared. Rather than clear it, you transfer to another card on a 0% transfer deal. Over the 0% term you add a bit more to the 'balance' and the term finishes. You transfer to another card (0% again) and do the same. Rinse and repeat until you have reached your credit threshold and you can't transfer the balance any further. Term runs out on credit card and you're suddenly hit with 22.2% on the 'balance' you've accumulated.

Sounds far fetched, but you'd be amazed how many people get themselves in this sort of mess...

a bit of discipline is required but credit cards are great. I've got around £65K of open credit at the moment and nearly all of that is invested in things that give me more than double the yield than I pay out in balance transfer fees. Same with the mortgage - currently have a base rate tracker mortgage of BOE base rate + 0.49% (0.99% in total at the moment) and rather than paying any capital off just put the capital payments into ISA accounts with the same bank where I earn 1.79% net interest. Effectively the bank are paying me 0.80% to take their money and give it back to them. Nuts!