![]() You don't need to be an 'investor' to invest in Singletrack: 6 days left: 95% of target - Find out more

You don't need to be an 'investor' to invest in Singletrack: 6 days left: 95% of target - Find out more

Thankfully no debt at all at 44 but then again i don't own a house, been in the same council now housing association bungalow for the past 20 odd years - thankfully it's in a really nice area of Galloway and rent is only £60 ish/week so i'm perfectly happy - no kids so what meagre amount at minimum wage i earn is mine to do with what i want - i've never earned enough to get a mortgage to buy a house but it's not something i've ever bothered about.

Some of the debt in this thread is horrific though, good luck to all so you can get it cleared

Inbred456 - MemberWhat amazes me is we have a decent income not that much debt. We save up mainly for things we need etc etc. People we know on modest incomes have just seemed to of gone mental spending. Brand new cars extensions multiple foreign holidays!!!!! How the bloody hell is that possible!

Perhaps their income isn't as modest as you think, when was the last time someone really said "I earn exactly £x a year".

When it comes to personal finances you might be amazed what's possible, but since 2007 at least it's now difficult to run up massive amounts of debt relative to your income, no more self-certing a mortgage 10 times your income, no more 110% mortgages and blowing the surplus on a conservatory and a cruise, no more 2x times your salary on the credit card paying the min 5% each month and spending it again or a new car on HP every year and letting some fast talking finance manager hide the shortfall from the last one in the cost of the new one.

Some people save well, some people spend well and some people do both, some people inherit pots of money, some people get 5 and the bonus ball and don't tell a soul. I don't believe there's a right, or wrong answer to how much debt you should have, how much you should spend, how much you should save - some people spend and save like there's no tomorrow, some people spend and save like they're going to live forever.

Sometimes though the answer isn't their income or their expenditure, but their circumstances - one of my closest friends has a AMG Merc, seemingly just to drive to the trail centres at the weekend, he's just changed his very, very nice Carbon MTB for the latest one of the same model because it's a bit different and doesn't seem to worry about money at all - lucky him, my Bike is old and knackered, my Car comes with my job and I'm broke most of the time - I don't know how much he earns exactly - but I'd guess it's +/- 10% of my income, I don't begrudge it - I've got a Wife and 2 kids to support and he doesn't - AMG's are thirsty, but they're cheap as chips compared to Childcare fees - I could probably lease a Maserati (where I got the idea for one of them I don't know) for the cost of keeping my Daughter safe whilst I work to pay for it.

Not all personal debt is caused by splurging on big ticket luxury items, just to let you know.

dazh - Member

Why are some people not including mortgages in their debt burden BTW?

Partially it's because it's debt secured against an (generally) appreciating asset and if I had to I could sell it cover my debt and recover any equity.

But mainly unless you are in the extremely fortunate position of owning outright you have a monthly cashflow liability for housing anyway be it mortgage repayment or rent and around here the difference is SFA. If I didn't have a mortgage I'd not have more money every month, I'd still have a contractual obligation to pay someone an amount for a fixed period if I wanted a roof over my head and that money would be doing nothing.

I think that makes it reasonable to consider differently to 'typical' unsecured debt in the form of loans, CCs, etc.

too true Mr grips, but this is STW...

(how many woodburners/trips to whistler/Vw T5's have been paid for with loans and credit cards i wonder? No doubt most of us pay for our toys with our enormous christmas bonuses, but i'm sure there'll be a few struggling to keep up...)

dazh - MemberWhy are some people not including mortgages in their debt burden BTW?

1. You've got to live somewhere.

2. Mortgage payments are often less than similar rent.

3. Paying rent is a short term view - you are paying your landlord's rent and won't have an asset at the end.

Mid-20s, no debt, 4x salary in savings and separate deposit fund (without help still a good 5 years off buying a house).

Noticed something interesting at the Xc race the other day.

There seemed to be two distinct types of rider;

1. Bangernomics/functional old car

2. Expensive '15/16 reg van, VAG, camper

They all had several thousand pounds worth of bike strapped to them though.

There was a distinct lack of middle ground in both car value and bike value.

It makes me wonder which of these two group (in general) have more unsecured/personal debt?

as opposed to using leverage to buy more of something that's appreciating in value

And people wonder why house-price bubbles happen! Mortgages are obviously the safest and best form of debt to have, but it doesn't mean you can disregard them as a debt. You don't own the house until the debt is gone, in that time a lot of things can happen, recessions, price bubbles bursting, ill health, negative equity, deflation, credit squeezes etc. All of those can combine in various ways to cause you to miss repayments and lose your property. Losing a house with half the mortgage paid off is a lot more painful than having a maxed out credit card.

Interesting. About £15k of debt for me. Don't have a mortgage, always rented. I'm 33. £10k is an unsecured personal loan that is for stuff I know longer own (cars, bikes, other material stuff et al) and about £5k on credit cards. If I continue the payment plan I've been on for the last 5-6 years, it'll all be gone in 2 years.

I've made some stupid decisions.

Oh, and I have zero savings, never have.

We're in our mid 30s and no debt, but we're getting another mortgage and bigger house. Should hopefully be back to no debt again in around 7 year's time though.

I've never lived with the idea that loans = money. I've always viewed life with the thinking that if you want something you need to gather enough money to have it. And we're very comfortable. Felt so great to have my boy born into a home that's not worried about money, simply because we don't spend lots.

Paying rent is a short term view - you are paying your landlord's rent and won't have an asset at the end.

Assuming house prices rise and rent is more than return that could be had by buying other assets such as equities. The reason so many of us have done well out of property ownership is the combination of leverage and price increases.

All interesting, 200k mortgage, but only 10 years left. No loans, no credit cards, couple of pcps for cars £500.

Nowt in savings, pension shite, just focus on getting mortgage paid as quickly as I can.

1. Bangernomics/functional old car

2. Expensive '15/16 reg van, VAG, camper

They all had several thousand pounds worth of bike strapped to them though.There was a distinct lack of middle ground in both car value and bike value.

It makes me wonder which of these two group (in general) have more unsecured/personal debt?

Someone I encountered recently through work has all the trappings... big house in Cheshire, mahoosive merc with the obligatory private plate, Trophy wife (who doesn't work but does shop) kids in a posh fee paying school. etc, etc.....

A colleague who knows him well said he's panicking at the moment as, as well as servicing his ****ing enormous mortgage, car loans etc etc, he personally (not his wife, just him. God knows what she's got also) has over 75 grand of debt on various credit cards 😯

Now to me, thats the tipping point. Is that your problem? Or the banks?

£560k on Mortgage, nothing anywhere else (probably £35k or so in a couple of savings accounts). Fortunately young enough to have it hopefully all covered in time for retirement 😛

75 grand of debt on various credit cards

0% balance transfer out of the question on that amount I'd guess 😯

Frankly this whole thread is rather vulgar IMO 😐 as my mum would say 😉

And people wonder why house-price bubbles

I'm not convinced you can get bubbles in something people actually need.

Now to me, thats the tipping point. Is that your problem? Or the banks?

It's not the bank's, but as a bleeding heart lefty, I'd say there is a societal responsibility somewhere. Actually no that's b******. He deserves to go under, and it will be the most valuable lesson he ever learns.

I've similar examples of people I know, including the couple who live in Dubai who have 200k credit card debts despite the fact that the husband earns a 300k a year tax-free. And the people who bought a house for 80k in the 90s who now have a 25 year 180k mortgage and are living in the same house with negative equity and complain about being 'trapped'. Not to mention the boy-racer I know who is paying for two cars he's now written off after driving like a dick. This is what happens when stupid people are allowed to do things they don't understand.

Frankly this whole thread is rather vulgar IMO

It's the [i]"Not wanting to talk about money because it is rather vulgar"[/i] thing that gets people into trouble in my opinion.

People being open and honest about earnings and debts can be pretty useful. Why dismiss other peoples life experiences as rude?

It may be vulgar, but it's making me feel better!

Someone I encountered recently through work has all the trappings... big house in Cheshire, mahoosive merc with the obligatory private plate, Trophy wife (who doesn't work but does shop) kids in a posh fee paying school. etc, etc.....A colleague who knows him well said he's panicking at the moment as, as well as servicing his ****ing enormous mortgage, car loans etc etc, he personally (not his wife, just him. God knows what she's got also) has over 75 grand of debt on various credit cards

Now to me, thats the tipping point. Is that your problem? Or the banks?

That sort of thing happened A LOT in the 2000s (I worked in finance for posh types for a long time and got to see peoples income and expenditure) and people got away with it by constantly remortgaging and 'releasing equity' to pay off the credit cards etc and starting the cycle all over again.

Nowadays it's not supposed to be possible either 1) the Banks they owe the money to haven't taken a proper view of their income and expenditure and have lent too much - that would be their problem 2) he's lied about his income / expenditure and it's his problem.

Either way, the end result is the same, as complex and brutal as it can be sometimes the laws on personal finance in the UK are fair, if he cannot control his spending there will come a point when he can't borrow another £ and it will all come to a grinding halt - I've seen it happen, people who seem to be very rich, earn very good money and live in very good houses - suddenly hit a wall - they're skint, their cards are maxed, they've got no cash left and they can't fill the 4x4 or buy food - I've had to tell people in a roundabout way they not only can't they have the 911 they want to finance, they are all but bankrupt and their outgoings are higher than their income and when they run out of credit - they can't buy food - the look of shock on their face when they realise that for all the houses/flat they think they own, but they've spent the equity on the next no-lose-gamble property deal, the 0% transfer deals on their credit cards which made it all free and cheap loans they're not actually rich at all, they're completely and utterly broke.

But as I said at above, the system is fair - if they cannot pay, they don't have to - but they have to admit to a judge that they cannot manage their own finances and they'll take all their assets, sell them and split the proceeds between their creditors - they'll all lose, but if they did their job properly they wouldn't have let things get that far.

When the banks fell, the Government of the day imposed new rules before they allowed the bail outs - in short it was to save us all from ourselves - Banks are required to check whether someone can afford to do, what they want to do - this meant the silly ones couldn't borrow any more than they should and they had a 0% base rate to ease things whilst they got their affairs in order - they've had 8 years to do it now, no doubt when rates finally rise again some people will be cursing their luck and crying off to the Bankruptcy court - but they've only got themselves to blame.

I'm not convinced you can get bubbles in something people actually need.

The hundreds of thousands who were repossessed in the 80s and the millions in the US who were repossessed after 2008 would probably disagree 🙂

Ex wife left me with £26K debt after our business got swallowed up in the divorce... thankfully didn't go bankrupt and worked my ass off to clear it.. 10 years later its a lot simpler £900 on an interest free card but savings can cover it, no mortgage and we paid the car off last year. Being self employed has made me more thoughtful with money and where it comes from.

In a previous job, we would sell electronic kit to customers, when they were refused finance after appearing as a dead cert sale the reasons would make your hair stand on end. The level of debt for some was staggering.

Interesting how your attitude to debt changes over the years. I've recently managed to clear our unsecured debts entirely leaving us with just a mortgage. We gave a great big collective sigh and agreed we'd do our best to never get in (unsecurd) debt again. In my early 20s the then gf and I used to ring up the CC company, increase our spending limit and then go to the offy. We could not care less.

As warren Buffett said when the sea goes out you find out who was swimming naked.

No debt and the Mrs owes me the £80 quid I paid to the lbs for repairs to her bike yesterday

As warren Buffett said when the sea goes out you find out who was swimming naked.

Not being vulgar, I'll not post my debt... But if the sea goes out, I'll not be in my boardies... :P!

Business loan that's 4 years into 25, SE England mortgage, wife and 2 kids, 39 and going grey...

If it all works, I'll be laughing in 20-30 years time!

I was mortgage free at 33. Then last year we moved to larger detached house, so a decent sized mortgage now.

No other debts though. I was quite bad with money in my 20s, racking up several £x000s on loans and CCs. Got my act together and squared them up before I hit 30.

I was mortgage free at 34...although tbf I didnt own a house either.

I was mortgage free at 34...although tbf I didnt own a house either.

🙂

In addition to salary, value of house, etc. please could everyone describe the size of their penis too ?

Because that's what this thread is [i]really[/i] about, isn't it ?

My penis is as big as my debt.

Massive and keeps me awake at night.

^ two post in a row 😆

Age 37, only debt is about £100k mortgage on a £200k house. Paying off over £1k per month which would clear it in 11-12 years. Pension contributions sitting at about £70k, £20k+ in cash savings and about £10k in a s&s ISA.

Last consumer debt was a loan for a car (not the full value, the difference between my savings and the price) 8 years ago. And a bike I bought on 0% finance over 12 months maybe 5 years ago because the money was earning interest while I paid it off.

I've got some savings and a pension....WTF happened to me, man?

Yeah, but how big is your fella? 🙂

Seriously, what a dreadful thread!

Bout the same as my savings

[img]  [/img]

[/img]

Actually, just realised something. After being deep in the red overall for most of my life, lately the equity in my house together with my pension pot outstrips my debt by a big margin. So maybe it's not so bad after all! I might be worth something net!

We've decided to kill the mortgage whilst interest rates are low. I'm 39 and have 8 years to go on the mortgage, we only took it out 5 years ago. No credit cards, no store cards etc etc... we would love a new kitchen, a new bike etc, but we've agreed to save for it and if we cant afford it, wait until we can.

I have friends on the other hand who have £300k mortgages, a car on the drip, massive holidays and i know for fact they cannot afford it. No savings, no real pension conributions. A car crash waiting to happen, but there's bloody loads out there like that. It would send me to an early grave personally!

Debt is only truly debt if the value of your assets is less than the money you owe. This is why Farmers always look like they are loaded (well at least while agricultural land is £10k an acre) debt is only relevant to circumstance and assets.

Personal finances in general are complicated. If anyone is genuinely having sleepless nights about their circumstances and debt, then it is[b] they[/b] who should have a voice on this thread, and hopefully would get advice/support on a way out of it.

Not stealth blah-blah-ing about how much you 'have'.

That wouldn't get much traction on here though, would it?

savings, pension, no mortgage, no personal debt. 6 year old bike, and 8 year old car

I've done this wrong haven't I?

I agree this thread may be a vehicle for some to wallet wave but it does serve a bloody useful purpose too.

As P-Jay has said, I have also looked at folks who "had it all" locally. Through work I had to deal with a couple who lived in THE executive development, had the cars, clothes, holdays etc. Turned out it was all funded by nearly £300k of debt, about £100k of which was unsecured. Property market crashed and their goose was cooked.

That was my epiphany and realised it's just smoke, mirrors and debt with a lot of people and don't get sucked into debt yourself trying to keep up. You're not "doing it wrong".

Kids and childcare is a killer. In my early to mid 30's it really felt like I was slogging my guts out just to pay bills but I found it does get easier.

For those that are seriously worried about their debt then speak to someone like [url= http://www.stepchange.org/ ]Stepchange[/url].

They are incredibly helpful and not judgemental. I got into a whole heap of trouble with over £40K of CC debt and £30K of unsecured loans on top of a £190K mortgage.

With the help of Stepchange and a DMP it is all paid back and other than the mortgage which now stands at around £140K on a £250K house I have no outstanding debts.

My Credit Score is probably as bad as it gets but that no longer matters really as we save for everything.

Don't be too proud to ask for help. I wish I'd done it sooner.

loads, but YOLO, no one says on their death bed "i wish id been more frugal"

loads, but YOLO, no one says on their death bed "i wish id been more frugal"

I'm sure some do.

maybe their kids do when they have to get a loan to pay for their funeral

None. Very pessimistic about asset values.

I know what you mean Jammers. I frequently lie awake all night fretting over asset values. It's the cross we all have to bear.

I don't like the idea of any kind of debt. I have a student loan (though I see that more as a tax) and I have been deep into my overdraft in the past. But outside of that I have never owned a credit card, wouldn;t even know how to buy anything on credit, only had one loan and regretted it, and if I want to buy anything I make sure I have the money for it first.

Don't know if that's a good or a bad thing really. I know I could own a lot more stuff. Drive some nice cars, live in a nice house. But at the same time I'm pretty sure I would be more stressed about it all.

Never liked having to pay companies (banks) to service debt so by 29 I was mortgage free, 34 I bought another house but didn't borrow a penny. I have a nice car, a few nice bikes and more importantly a happy life. Was planning to retire at 50 but then had kids (well one child) so will work until their education is over to help and not let her adult life start in debt.

I don't like the idea of any kind of debt.

On the other hand, we love it! 🙄

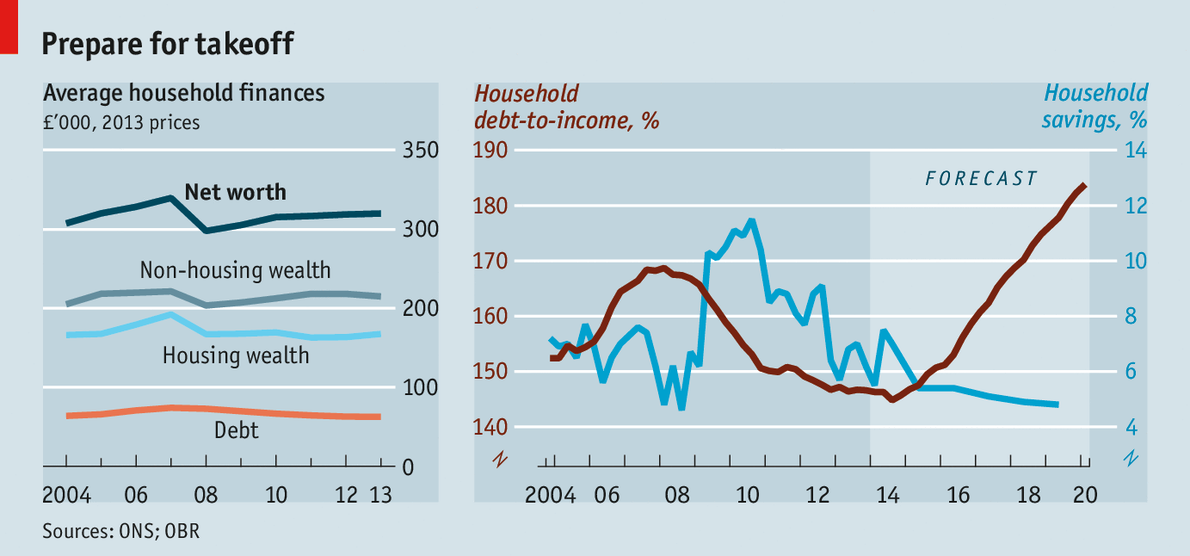

8 years into a still unresolved debt crisis and this chart is terrifying...

[img]  [/img]

[/img]

To be fair we don't know the driver of the increase. I asked a friend of mine who works as a data analyst at the Bank of England and he said it was availability of credit. Looking at the sums being doled out in massive mortgages and especially BTL, and in PCP deals on cars, I suspect that contributes a lot to this chart. Maybe some people are living off credit just to pay bills, I don't know.

I guess there's plenty my mate knows about the state of things but can't tell me, sadly! He doesn't subscribe to the 'economic growth forever' thesis, I know that.

We're going to have to pay it all back one day... or in the case of mortgages, we'll just force the younger generation into a lifetime of crippling debt to keep the whole pyramid going a little longer... I can't quite believe we've got ourselves into such a dire place in such a short space of time.

It's interesting that we've been stuck on emergency low interest rates since 2008 to help keep the debt from overwhelming us but those rates are now playing havoc with banks' ability to make a profit - so we're stuck. Raise rates and a load of bad debts lead to a banking collapse, keep rates as they are and see debt increase still further and banks crash as they're unable to make a profit!

Brooess - on closer inspection I see nothing terrifying on those charts. It shows a drop in people's debt:earnings in recent years, and the alarming spike is just a forecast with a compressed y-axis to make it look sensationalist.

3 years out of date also.

Really interesting thread, debts a big part of a lot of people's life's

debt is sold as freedom, exotic holidays, nice cars, etc etc. In reality it's exactly the opposite. Some time ago I read about how with the advent of production lines in USA they had trouble getting anyone to work on them (Henry Ford had to employ 10 people for each job as 9 would walk out)

The answer was, as a leading economist put it "to keep people greying in the harness" the answer was debt. What we know as marketing was invented at the same time

Myself, made some mistakes, less than 10 years ago had a 180k interest only mortgage plus 10k in cc etc. This year I will be completely debt free, including mortgaged (downsized). TBH i don't feel massively different, but I certainly sleep better. It is allowing for my mid life crisis mind, in a couple of years my daughter is off on a gap year, I'm also going to take a year out travelling, with the house rented I won't feel like I have to come back

[i] loads, but YOLO, no one says on their death bed "i wish id been more frugal"

I'm sure some do.

[/i]

I heard this yesterday;

"He died unexpectedly solvent"

Not sure if I want to die with massive debts, massive savings or a clean slate, really.

the only thing that stops me going with the last option is that I reckon my kids will never be able to afford a house in SE England unless I pop my clogs and leave them a big chunk of money.

Not sure if I want to die with massive debts, massive savings or a clean slate, really.

seeing what my family had to deal with when my gran died unexpectedly and young its not as simple as rack up debts and the debt dies with the person.....can make life very difficult for surviving partners ESP when they come a knocking for the assets back (ie house) to service the debts left behind...

So maybe it's not so bad after all! I might be worth something net!

You have children right? By the time you've paid their deposits for a house plus subsidised their poverty wages, you'll be back in debt again 😉

the only thing that stops me going with the last option is that I reckon my kids will never be able to afford a house in SE England unless I pop my clogs and leave them a big chunk of money.

Life & Critical Illness Insurance helps cover that eventuality.

Me being diagnosed with something terminal and then popping my clogs is probably the best outcome all round for my family 😯

Me being diagnosed with something terminal and then popping my clogs is probably the best outcome all round for my family

Aint that the truth. Mortgage done and £400k-500k in the bank for them.... it's all good.

Not ideal for me though I have to say.

wwaswas - Memberloads, but YOLO, no one says on their death bed "i wish id been more frugal"

I'm sure some do.

I heard this yesterday;

"He died unexpectedly solvent"

Not sure if I want to die with massive debts, massive savings or a clean slate, really.

the only thing that stops me going with the last option is that I reckon my kids will never be able to afford a house in SE England unless I pop my clogs and leave them a big chunk of money.

"I want the last cheque I write to bounce"

I also like the idea of passing something onto my kids, but I think times have changed - No I don't want them to have to pay for my funeral, but hopefully they'll be looking at retirement themselves before I shuffle off, rather than trying to buy a place or start a business or whatever.

In regards to the whole YOLO thing, it's absolutely true - some people refuse to admit they're going to die one day and are always looking towards the future and they'll be the richest guy in the Cemetery, but on the other hand, if you pick through the thinly veiled boast posts there's a fairly common theme of people who go a bit mad in their twenties, end up in a world of pain and then spend their 30s trying to fix it all - it's a shit place to be.

Personally, to be as happy as I can be, or perhaps a stress free as possible financially I'd like to have a place of our own with a mortgage, a months salary in savings and zero other debt - the last 6 years for me has been tough, starting a family, getting married and made redundant twice - it seems almost silly, but having a nice buffer of disposable income each month, makes me happy, happier than having lots of things and a credit card bill that sucks all my 'fun money' up - I'm not quite there yet, but with luck I will be soon.

I remember growing up in the 1980s with parents worried about mortgage interest rates of 15% and having a family kitchen table conversation about potentially having to move to a smaller house. I remember my parents "borrowing" from my 9-year-old savings and that when Birmingham Midshires (like many de-mutualised building societies) gave me a windfall, that I got £50 while the rest disappeared to presumably keep a roof over our heads.

That was all in quite a middle class household (my dad was a uni lecturer) and it really shaped my attitude to money and debt - as did typing thousands of case letters for 2 years about people's debts when I worked at a Citizens Advice Bureau as a student. Many people are just a short illness away from penury, stress and strife; often for much lower debts than you'd have thought would trouble them.

My grandparents - and especially my grandad, who grew up in the Depression and walked from Sunderland to London in the 30s to find a job - always said that debt was a terrible thing and couldn't understand why my parents took a mortgage (which was very much the norm by the 1980s). They had seen people endure serious hardships and detested the "never never". They'd always rented houses and took great pleasure in occasionally buying nice things (new cars, clothes) from savings ... working class people who did well for themselves and proudly achieved independence in many senses of the word. They didn't have any property assets, just enough cash savings and pensions to live comfortably.

I'm now close to old money. I'm talking about people who are squillionaires, but drive around in diesel Golfs and whose soft furnishings and clothes are patched-up and rarely replaced - but when they are, it's with a quality item bought for cash. Money is vulgar; assets and markets are more of interest. Expenditure from savings is only for private schooling or houses: everything else is frivolous.

I've learned to consider that if today's debt-led consumer society works for some people, then that's great. But do be sure to know who's in control and to prepare adequately for the downsides.

48 with a £200k mortgage on a £600k house, £4k on an interest free credit card and £189 a month for another 18 months paying back an overpayment to HMRC (interest free so no need to pay off any quicker) + a few thousand in savings right now, but will be using some for house improvements over the next year.

Next year when the credit card and HMRC debts are paid off in full I will divert all that money into mortgage overpayments and aim to pay off by the time I am 55 - then continue to pay the same amount into additional retirement savings.

When I finally retire I then plan to downsize and buy two houses - one for my wife & I, the other as a rental income for our retirement.

When we both kark it, we then have a house each for our two daughters.

Or, as said above, I go now and use the insurance policies to set my wife and kids up instead....

Interesting to read the answers, surprised how open and honest some people are. Also surprised there aren't more answers of huge debt - perhaps these people have chosen not to answer?

The thing about the numbers being mentioned above is it is only part of the picture. A single person living in a shared flat earning £250k per year with £10k of debt is very different to a single parent of 4 working part time on £12k per year with the same amount of debt.

"He died unexpectedly solvent"

Sniffing glue?

I left uni in 2004 with about £15k worth of student loan, a maxed out overdraft and credit card and a few loans/finance agreements, so maybe £20k+.

Managed to buy my first house with my GF in 2011 after I got made redundant in 2010 with my redundancey money, having been lucky enough to find a new job pretty quickly.

Over the next 5 years or so, our house went up in value and we managed to clear most of our debt off, as well as getting married along the way.

We've just sold our first house for £105k (paid £78k) and brought a new build for £253k plus about £6k in extras using the help to buy scheme.

I'm now 33, and we are debt free minus the mortgage and my student loan. So currently owe £190k in mortgage and 20% equity to the government, currently about £50k. we've also got about £13k left over from the house move in the bank.

Hoping that in 5 years time we'll owe between £180-£190k on the mortgage, but will have paid the h2b loan off and my student loan.

Currently don't really have a pension, but am planning on investing a decent percentage once my company pension scheme starts next month.

I'm hoping to get nothing from either of my parents, want them to live long enough to make the most of it, they were skint most of the way through my childhood and probably into my early 20's. And I'm probably more financially stable now in my 40's than either of them ever were, up to the point they retired.I also like the idea of passing something onto my kids

I know one of them is mortgage free, and the other has a bigger mortgage than i do. (not to mention less savings and a smaller income)

I have two mortgages: one on the books with the bank, and one off the books with the inlaws. Oh and a PCP on a car.

But PCPs on cars don't count if the rate is cheap enough - you pay for the depreciation on every car*, so PCP is a means of managing cashflow of the same at an acceptable interest rate.

*Obviously not true for a number of classics and not so classics given the recent pensions-driven car boom.

"But PCPs on cars don't count if the rate is cheap enough "

who makes up these justifications for debt ? Is there a copy in print ? i'd like to see what i can acceptably have debt on.

[i]what i can acceptably have debt on. [/i]

bicycles?

excellent im off to fill my boots at the bike shop.

Highball 29er here i come 😀

I'm adding money to my mortgage in order to put money into a couple of 123 a/cs, will cost me 1% and will get 3% and it's all tax free 🙂

In what way is the 3% tax free?

I think when I was younger I wanted everything, and genuinely got a bit of high from owning something cool that no one else I knew had, but I've now realised that the novelty/high wears off fast!

I traded in loads of nice motorbikes in my 20s and "upgraded" to faster and nicer bikes every year or 9 months, loosing loads each time. I now know that any half-decent mid+ engine bike gives you the same pleasure and does the same job as a £12k BMW 1300cc super tourer!

I hate to think what I would have owed if I was into cars rather than bikes and did the same thing...

I've never got the holiday thing though, I like stuff, rather than experiences (that's probably a whole other type of issue I have!), so wouldn't borrow for holidays.

I don't think there's anything wrong with borrowing, but it seems some can live with it and others cant. After feeling trapped at a crap job because it paid well, and I needed the cash to make monthly payments, I don't want it again personally.

clearing mortgages is one option, but there are better returns for the same money - like your pension. The tax advantages are pretty good. Just keep an open mind on return on capital. You may think your doing well as your pension and retirement slip away

In what way is the 3% tax free?

From April, up to £1000 interest pa is tax free, if you pay std rate tax.

I don't think there's anything wrong with borrowing,

There isn't necessarily. It's when you do it to the scale we have (and now the Chinese appear to be too) that it becomes the systemic problem that it now has become.

It also depends what you get into debt for - something which is an investment for the future which provides a firm financial return (e.g. a student loan which allows you to get a better paid job and increases your lifetime earnings is a productive use of that debt. Companies will use debt to fund investments in machinery and people to drive future growth, revenue and profits)

However, our consumer debt appears to have mainly been run up spanking cash on shiny things and general consumerism (mainly depreciating assets), and BTL property (making heroic assumptions about ever-increasing house prices) or just normal property (boosting it to such a level in London and the SE that the repayments dominate our disposable incomes and leave nothing left for the real economy and therefore leave us with constricted economic growth over the long term).

The scale of our debt is the real problem - it'll be a burden for a very long time and hold back economic growth and living standards whilst we pay it back. Assuming it doesn't take us under again in the meantime. The nature of what we've spent the money on is also a problem as it largely will produce no longer term economic benefit.

We've been really quite stupid...

there's a fairly common theme of people who go a bit mad in their twenties, end up in a world of pain and then spend their 30s trying to fix it all - it's a shit place to be.

I've got £1200 left of my early/mid 20's debt and I'm 35, its in an interest free repayment plan with Cabot, i could pay it off tomorrow, but id notice the £1200 gone, i barely notice the £50 DD that comes out a lot was wasted (shit car, high insurance) some paid to fund a 7 month sabbatical from work playing on boards and bikes in the Alps, i had a good time, but not a great time as one eye was on the ever increasing pile of full credit cards with zero income to pay them, ended up back in my old job, single, but i think it changed me for the better, i like to think it did, however there were dark days but I'm quite the optimist 😆

I'm at the other end of most people's situation.

From 20 to about 55, raised a family of three with my wife, never had much spare cash or savings, wife stayed home to raise the children.

Even had a spell of four years without a car as we didn't want any more debt.

Now 61, retired, no debt at all.

My savings, pension fund our modest lifestyle. No work, got back cycling in the last year, went a bit daft buying and selling some bikes which didn't suit.

As a result, realised that having time to just enjoy riding, no debt, and a future of no more borrowing or working is very good.

Can't believe how much some of the forum members owe on a mortgage though, would have worried me to death.

Always worked all my life, but very few people are in control of their work and employment security.

I was made redundant twice.