![]() You don't need to be an 'investor' to invest in Singletrack: 6 days left: 95% of target - Find out more

You don't need to be an 'investor' to invest in Singletrack: 6 days left: 95% of target - Find out more

Hi all,

I'm dealing with an estate and one of the beneficiaries is not allowed thier share until they turn 21 in a few years.

Can I just stick it into say a 1yr fixed savings account or similar? would I be able to put it in thier name as opposed to mine for transparency and financial seperation purposes?

If the account is in the beneficiaries name though, whats to stop them accessing the funds before they 'come of age'?

I guess so, but I'd need to open the account before the money is available so I can have the solicitor dealing with the estate admin, send it straight there from the estate account...

I could have the solicitor do that but they would charge time, so seems a bit silly for the sake of just opening a bank account if I can do that...they have said: This would usually be held by the executor. An account would need to be set up by the Executor for the money to be held for her.

Any ideas?

Thanks

Is this not what trusts are for?

On what basis are they not allowed the money? Assuming the will instructs this, doesn’t it also say what is to be done with the money in the meantime?

I’d consider a deed of variation to alter that part of it, depending what you mean by “a few years” (less than 3, for sure, more than 10, perhaps not). Since no-one else is damaged, I’d think it should be possible.

If its in their name they can access it, maybe worth a chat with the bank. Have you money already in the executors account - MrsF still has money held in her dad's executor's account jus tin case any bills come through (FIL died 8 years ago, MIL last year).

I wouldn’t be prepared to hold the money myself for a lengthy period of time as an executor. You want the job done, finished, as soon as reasonably possibly. You may be personally liable for any failure to satisfy the distribution of assets.

An account that needs both your signatures to protect both of you? That way neither of you can access it alone. As well as protecting the money you need to protect yourself here. Money does weird things to folk.

MrsTJ left a significant sum to our godless grandchild for his education. Its in an account that needs his uncles signature to access it ( no age restriction but she didn't want it wasted on C&H) the uncle I trust implicitly at least in part because he is richer than the rest of us.

It all depends a great deal on the family dynamics and how much money it is.

Is this not what trusts are for

Ahh I guess so, but doing a google search, it seems trust funds aren't as easily comparable to see interest rates, terms etc. as regular savings and ISA accounts are...you can just go onto MSE and select what's suitable, it doesn't seem to be the case with trust funds.

Assuming the will instructs this, doesn’t it also say what is to be done with the money in the meantime?

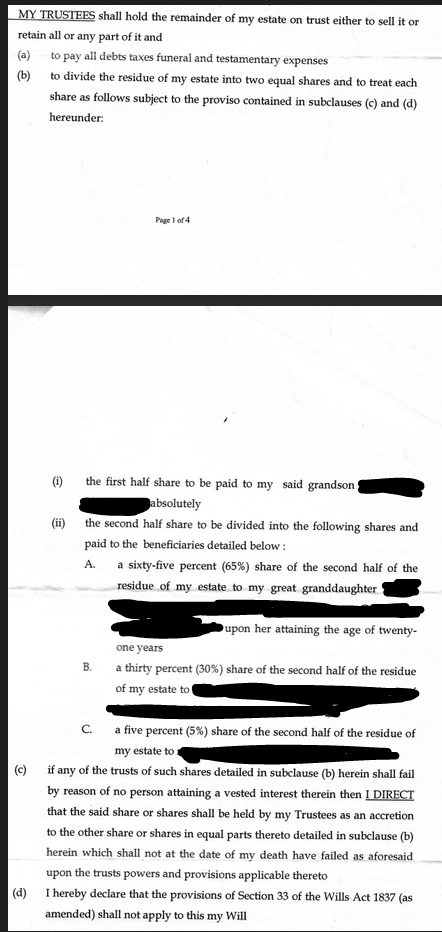

Yes but the will just states it should be held/retained by me as trustee/executor of the estate until they are 21yo....

I don't think you can hold it till they are 21.

18 was the max age when we had to do it a couple of years ago.

We had a solicitor dealing with the estate and even with that the conclusion was it was easier to leave it to his mother to look after.

How well do you know the person?

For me it would be all about keeping it simple and protecting folk hence a savings account with the best interest you can find in her name with you as joint signature on the account so she can only access it with your consent then explain to her why its been done like this

I am not a lawyer!

Pretty much what tj says but maybe speak to a bank & see if they can suggest anything sensible.

Thanks for the replies so far..!

Have you money already in the executors account

The solicitor I've appointed to do the admin currently holds everything in ther account, but they will be looking to distribute in a few months once everything is finalised..they are charging a fixed fee to come out of the estate so I assume they will be wanting to be done and dusted with it at that point, or they would charge to take care of any trust arrangements etc.

I wouldn’t be prepared to hold the money myself for a lengthy period of time as an executor.

It will be for about a year and a half so I thought a 1 year fixed savings account would be easiest, and I can compare accounts online to get one with decent interest/terms.

I think it will be about 20-30k, but the estate isn't finalised yet, so there's interest to be added and costs/expenses to be deducted.

You have a duty as executor to look after the money on her behalf - so there might be better options than a bog-standard low-interest account.

You might get a better rate on a three-year bond type product if you shop around. Just make sure that all the details and logins are kept somewhere safe so she can access the money if you go under a bus in the meantime.

Thanks all, this seems easiest...

For me it would be all about keeping it simple and protecting folk hence a savings account with the best interest you can find in her name with you as joint signature on the account so she can only access it with your consent then explain to her why its been done like this

Just not sure about having my name on it - could it affect my tax affairs? I guess not as it's inheritence and any tax due is alredy paid out of the estate?

You might get a better rate on a three-year bond type product if you shop around

It's only for about 18 months and then I'm required to release it. The will states that I must 'hold' the money until then.

her name on the account. Her account, her money. You are just a co signer for it. You need real advice tho. The bank can probably help with this stuff.

her name on the account. Her account, her money. You are just a co signer for it. You need real advice tho. The bank can probably help with this stuff.

Yes that makes sense, thanks, and when she turns 21, I can just remove myself as co-signatory, and job done I guess.

looking at MSE, you can get a 1yr fixed savings account at about 5.9% interest, so that seems easiest whilst fulfilling my duty to 'look after it & invest it responsibly', or whatever the legalese term for that is.

I agree with TJ's suggestion and your 1 year fixed rate plan. I think that would show your intent to look after and invest appropriately.

Only caveat would be regarding the sums involved. Could there be a tax implication on the interest earned? If so maybe a fixed rate cash isa is a better option

Also check you can set up the ac and add money later, as your post seems to suggest you won't be doing both simultaneously

You are paying the solicitor to administer the estate so I would expect them to guide you, if requested, on what you can/cannot do with the beneficiary's inheritance; this would not be financial advice as that is not what solicitors do.

As for the age at which the beneficiary inherits, that should be stated as part of the 'Beneficial Residue of Trust' section of the Will - you have stated 21; the same section would, typically, include a statement to the effect that the money is to be held in trust.

The named trustee(s) to the Will are responsible for managing the trust.

The suggestion of a deed of variation to amend this is, IMO, a non-starter.

I suggest you work up a short list of questions for the solicitor and use their responses to help you decide what to do.

I've recently revised my Will and discussed a number of points with my solicitor regarding grandchildren inheritances - including trustees, their responsibilities and how best to ensure those responsibilities are carried out.

No doubt this’ll fail but I feel obliged to try:

Hahah!!! thats why I want to do it properly...

Or I could just buy a load of crypto with it...gainz!!!!*

As for the age at which the beneficiary inherits, that should be stated as part of the ‘Beneficial Residue of Trust’ section of the Will – you have stated 21; the same section would, typically, include a statement to the effect that the money is to be held in trust.

The named trustee(s) to the Will are responsible for managing the trust.

Thanks.. yes it's pretty straight forwad, I don't see why a deed of variation would be required, and it would cost!

This is the relevent section of the will, for reference I am the grandson(and executor and trustee), and the great grand daughter is my neice.

her name on the account. Her account, her money. You are just a co signer for it.

This is not the right approach. It's also more complicated. You are supposed to have sole control until you can hand it over. Open a separate, interest-bearing bank account in your own name. When the kid reaches 21, give them the money.

This is not the right approach. It’s also more complicated. You are supposed to have sole control until you can hand it over. Open a separate, interest-bearing bank account in your own name. When the kid reaches 21, give them the money.

I get that, but if she cannot acess the account without my co-signature, then for all intents and purposes she can't do anything with it unless I get hit by a bus or something, at which point it won't be my problem any more, and she could show the will and take over the account ?

I'm not envisageing any fall outs or animosity, and she's already aware she has an inheritence that she can't have until shes's 21.

I just don't want to have to pay further cost from the estate to administrate a trust or whatever if a simple free to open 5.x%+ fixed term savings account will do the job, as the money only needs to be held for approximatly 18 months, if that makes sense.

Fair enough PCA - I did suggest getting real advice.

Yes, sorry, thanks PCA... I will speak to my bank in the first instance, as I'm sure it's not an uncommon occurence.

My bank only seems to be offering 5.3% on a 1yr fixed rate savings bond account, for example, and others are offering over 5.8%.

I'm probably overthinking this, I'll speak to my bank in the first instance, and I should be able to glean some info as to if this is an appropriate plan of action, and if yes, then I'll just shop around for an equivalent account that pays a bit more interest.

I believe she’ll be entitled to the interest arising from the trust. I’m not sure if this applies only in the case where you legally establish a trust, or also in the case where you are just de facto holding the money “in trust”. I’d still be very dubious about the latter in case anything goes tits up (eg bank crash, but also fraud) leaving you liable.

Given that she’s over 19 I really think the obvious solution is to change the will and give her the money asap if that’s at all possible. 21 is a stupid anachronism unless there is an advantage for a student to be poor these days. (There was when I was a student but that was decades back.)

An executor cannot change a will; neither can a beneficiary.

Either - or both - can challenge a will but that is a legal, time consuming and (probably) costly process.

Just let the clock run down until the beneficiary reaches 21; anything else seems pointless.

I believe she’ll be entitled to the interest arising from the trust. I’m not sure if this applies only in the case where you legally establish a trust, or also in the case where you are just de facto holding the money “in trust”. I’d still be very dubious about the latter in case anything goes tits up (eg bank crash, but also fraud) leaving you liable.

Given that she’s over 19 I really think the obvious solution is to change the will and give her the money asap if that’s at all possible. 21 is a stupid anachronism unless there is an advantage for a student to be poor these days. (There was when I was a student but that was decades back.)

I get your angle, but as executor I must, and will do as the will dictates... and it's only a matter of holding the money for about 18 months and putting it into a sensible account to get a bit of interest (for her) in the interim.

the obvious solution is to change the will and give her the money asap if that’s at all possible.

That would make no sense, as to change the will, will cost thousands.

And will not serve any purpose that I can think of. It's not a contested will, I'm just looking for the appropriate container to put her money into. As the will dictates I (as executor) cannot give it to her until she's 21, they are the wishes of my Nan, and I don't know my neice that well, but I know her well enough to know that she's not ready to have potentially 30k in cash. She probably won't be ready at 21, but that's not my choice to decide.

I am speaking with her mother (my late brothers ex girlfriend) and we are both of the opinion we should try to gently guide her into using it as a deposit for a small house, or some other sensible use of the money but once she hits 21, she gets the cash, simple as that.

It's entirley possilbe she could waste it on a few expensive hollidays and a fancy car and then it's gone, because that's exactly how I wasted a bunch of money when my mum died...

I am not going to go against the will, and I have no intention of doing so.

She's a typical 19yo..maybe she'll make better decicions when she's 21, rather than 19, but my hands are legaly tied in that respect.

Of course beneficiaries can change wills, very frequently do, and I doubt very much it would cost more than a few hundred at most. But anyway, you can work out how to hold the money for 18 months if you really want to.

Of course beneficiaries can change wills, very frequently do, and I doubt very much it would cost more than a few hundred at most. But anyway, you can work out how to hold the money for 18 months if you really want to.

No offence intended, but I think you are missing the point, you cannot change the will of the dead without a lot of cost, many thousands rather than a few hundred quid and that is not my intention, and not my nans will.

you can work out how to hold the money for 18 months if you really want to.

That is the question, what would be appropriate...

I'll speak to my bank and if they can open me up a 5.x% 1year 'locked' account, in the name of the niece that would seem the path of least effort, whilst still taking care of her share in a sensible way as executor.