https://monevator.com/what-is-a-sustainable-withdrawal-rate-for-a-world-portfolio/

for the 75k earning – I wasn’t questioning this, just stating that if you earn 75k when you retire, you probably want to have a 50k pension to not have significant loss of lifestyle – whereas at 50k income you’d be ‘happy’ with 30k.

Well if you've been shovelling 40k pa into the pension and a chunk of the rest into ISAs for years then you're not likely to notice a dip in lifestyle...

I can’t see where you’re coming from saying you need to earn 60-70% as much in retirement.

You wouldn't need to earn that percentage IMHO

My wife and I are both retired. We are on 50% of our final salary but take home c 65% of our 'last working months take home'. In real terms we are better off. We now have no mortgage, no longer pay a huge chunk into the pension, no longer pay NI and have chosen to drop to 1 car from 2, so lower monthly there. Lockdown has shown us what we could live on with no extras.

Planned properly, 6 weeks in Spain or Portugal in February/March can be done very cheaply so getting away from dull and dreary UK is easy enough.

Posh holidays? Not really my thing but easily do-able every couple of years if you really planned for it...same with a new bike etc.

Thinking about the above and yeah, I dont think I would need anywhere near what my current level of income is to have a lifestyle I would enjoy.

As has been mentioned the obvious big difference would be not having the mortgage and overpayments (soon to be pension payments) coming out - that's probably worth 30% just there. We bought the house we could afford a few promotions ago and never moved up as we got more money which puts us on a good footing there. Then as above lockdown has made me realise that the simple things and a slower paced life are enough to keep me happy, and as someone said a less manic goal orientated use of free time will be a saving. Not being bound to the school holidays makes those about a third of the price too, and my hobbies are all relatively cheap things like running, hiking, cooking etc

I've rung around the historic providers for the pension scheme at work and found I have a couple of amounts so I'm not starting from zero either which is good but looks like I have some work to do if I want to beat the mortgage, squirrel a ton away in pensions and have enough to bridge a gap from say maybe 52 to 57

no longer pay NI

Make sure you keep your NI payments up to date with voluntary contributions if you want to get the max state pension. A simple check on gov gateway will tell you if up to date or short

Make sure you keep your NI payments up to date with voluntary contributions if you want to get the max state pension. A simple check on gov gateway will tell you if up to date or short

For those of us who didn't 'waste' their years away drinking in the Uni Bar we're already well passed them - it's only 35 years.

This thread has really got me thinking.

I have got 4 pensions in total from 4 different employers - only one is currently being paid into & is the one that is the largest, so I tend to concentrate on what that will give me in my retirement.

I generally have money left over at the end of the month - normally not a ton of it, but some. Currently with lockdown restrictions & no commute, there is obviously more.

I am currently overpaying the mortgage by a modest amount, but constantly wonder about the worth of doing that with low interest rates. I could put that money in an investment ISA & make it work harder. It would also be available if needed, whereas the mortgage overpayments are gone once the payment is made.

Or I could put the money onto my pension but again, that money is then not available should the need arise.

The rest of the money gets chucked into random savings accounts - one for house renovation work that needs doing (new boiler soon, hall, stairs, landing redecorating & a new kitchen at some point) and another which is just a random savings pot. But they earn bugger all interest so seems like a foolish way of doing things.

I think I need to review all of my spending & have a bit of a re-jig.

For example, I'm currently paying £150 a month into childcare vouchers, but we barely have any childcare requirements. We envisage will we need to use after-school clubs in the future & probably for a few weeks during the summer holidays, but we have a current balance of over £3k of vouchers which should keep us going for a while.

Anyway - good thread this. Certainly gives some things to think about.

stumpy01

Eggs and baskets. Don't concentrate on any one 'investment' or investment type IMO.

have a look at LISAs as well if you want a blend of locked-in and not. LISA is better than an ISA for retirement saving (but worse than a pension) - but the advantage is you can take your cash out of a LISA at any point with a minimal cost (something like 4%) if you have to. There's a bunch of limits as to how much and who (under 50s, 4k a year) but its always good to get some free money from the government.

as for retirement spending, everyone's different. I imagine that going from 7 weeks a year of messing around in foreign countries to up to 52 will significantly increase my spending in the first 5-10 years, although it might well slow down after that.

LISAs

unfortunately for me (and others....)

Anyone aged 18 to 39 can open a LISA

I would look at pension contributions now as there is a chance tax relief will change in the budget.

I see my pension as long term savings now as I retire (60) in 14 years, and no other investment can come close to the 40% bonus of tax relief.

If you've got old DC pensions, folks, check the charges and investments - might well save a few bob transferring them to a low cost SIPP with a decent range of index trackers, ITs etc

For those of us who didn’t ‘waste’ their years away drinking in the Uni Bar we’re already well passed them – it’s only 35 years.

Assuming you didn't get caught up in the opted-out pensions that were the rage a few year ago that don't count towards your numbers IIRC (could be wrong).

I checked the gov website about my contributions (like you assuming I'd have my 35 years in in the next year or so). Apparently not, even though I was in full time PAYE employment it came up saying I'd only part paid in some of my early years (no idea how or why) so I've potentially three more year that I wasn't expecting and far too late to get it sorted.

I'm also a bit confused about the 35 years. The gov website says 34 full years so I assume it will tick over to 35 in the next tax year, April? Which will give me full allowance.

I certainly don't recall having a job and paying ni between 16 to 20 so not sure how it's hit 34 really.

There are exemptions and years that count without contributing. IIRC my two years at college (16-18) count, but my uni years don't count (although I got a partial credit for part time work)

Never mind - I misread.

Yes I wasnt clear it shows me as having 34 full years of contributions in the forecast portal.

34 years of full contributions

17 years to contribute before 5 April 2037

You do not have any gaps in your record.

Which is odd as i was in higher education till 20 or so & did some slacking off in my late 20's.

Good result though.

40% bonus of tax relief.

whilst the tax relief is good, its worth remembering that its only for the initial ~25% (tax free lump sum) + 3kpa (difference between state pension and tax free limits) of income - after that you're taxed at 20% or (less likely) 40% on your income - still good but not as good.

I think he was referring to the tax relief on the money paid in, rather than coming out.

– still good but not as good.

As what?

Just to the OP. I am retiring soon on about 1/4 of what you will have. I do not care that i will be skint. I will not be working

As what?

its not as good as 40% off. In fact, LISAs, VCTs, and EIS can all be more tax efficient depending on your cirucmstances

its not as good as 40% off

It really is. You pay money into into a pension. The government instantly adds 20%. Then when you do your tax return, you tell them you put money into a pension and then they give you another 20% (assuming you are paying higher rate, of course). Then you get the compound growth on that 20% until you draw on it. I don't really think you can beat that with any of your other options.

Wait what? As a paye employee I need to do a tax return?

I was auto opted out by work, had no choice so I still have 3 yrs to pay despite 40 yrs of contributions

@stumpy01 - re: childcare vouchers, sure you're aware but you can't turn them back into cash. I'd have a clear plan on when and how you're going to spend that £3k

I have £300 in vouchers sitting there now with no way of spending them. Youngest is going to senior school in September so no need for before/after clubs anymore. Only way I can think of using the money is on private tutors who may accept the vouchers

It really is. You pay money into into a pension. The government instantly adds 20%. Then when you do your tax return, you tell them you put money into a pension and then they give you another 20% (assuming you are paying higher rate, of course). Then you get the compound growth on that 20% until you draw on it. I don’t really think you can beat that with any of your other options.

Its not as good as 40% when you're taxed 20% on close to 75% of what you withdraw. Its much closer to 25%.

An seis has a 50% tax claim and an eis is 30%. Both of those significantly beat pensions from a pure tax perspective (although they are generally riskier investments)

I still have 3 yrs to pay despite 40 yrs of contributions

I'm in exactly the same position: years to go, contributions to make.

At today's rates, Grade 3 contributions would cost £2340 for 3 years worth, @ £15 p/w.

At least I have 11 years to decide if it's worth it, for £10 a week

This is a fascinating post. I am 55 tomorrow, working in a good job and decent salary, with a fairly poor private pension. No mortgage, nice house, 2 teenage kids, and moderate savings (a year of net income] plus a good planned inheritance which is unfortunately not too far distant.

I haven’t really thought much about all of this until this thread !

I take it you are retiring in just under 4 hours?

Is there a school of thought that you’re better to spend now while younger and fitter and can enjoy life, work till 67 and accept you’ll be poorer when less able to do the good stuff anyway.

There is, and that's fine if you are knackered by the time you reach 67. If you're fit and healthy though 20+ years on the bread line my not be much fun.

Is there a school of thought that you’re better to spend now while younger and fitter and can enjoy life, work till 67 and accept you’ll be poorer when less able to do the good stuff anyway

There is a balance. Whenever pensions comes up here it's often said that the best thing is to put as much as you can in as early as you can but when young there is so much to spend money on. I worked a bit then blew my savings on some traveling. Came back then did it again. Had some great trips at an age when I was happy to bum around. No regrets at all. Then came buying a house. Not much spare money when doing that. Once settled I've got into saving for the future. Definitely started late but not too late I hope. On track for early retirement.

I think the balance is tricky as mentioned. Also I think it is hard to curb lifestyle creep as earnings typically increase with age and experience. I try and put any pay increase into pension to avoid frittering it away.

Balance of ISA and pensions for me. ISA for the access before 55/57 and pensions for the tax relief. Probably around 15 years off for me but I have an overall pot size in mind to drawdown an annual income. At this point cash flow software would be useful to forecast the increase when state pension kicks in so you can afford to drawdown at a higher rate before the state commences.

Lots of variables in 15 years. One thing I’ll never forget a colleague saying to me when I was 20, “early contributions make the dough rise.” Very true and there is a reason Albert Einstein was a big fan of compound interest. https://www.aesinternational.com/blog/is-compound-interest-the-eighth-wonder-of-the-world

I blew all my money travelling when 30. I had to start again when I came back. I am still retiring at 60 but I do not live an extravagant lifestyle. Its going to be tricky living on my small pension but I can do it

For me the key is to live a sustainable life

Just an observation, many folks in here very focused on "retirement" as in stopping working. I think work in some form is really good for most people be it paid, a business or voluntary.

The real question for me is how do you fill your time during a winter like this unless you have plenty of cash? My Dad retired at 63 and basically sat on his arse until he passed away watching crap TV. My Father in Law also retired early and just drank away the time.

Maybe part time jobs setting up a small business help both financially and mentally?

Very similar thread here with some different ideas and perhaps more emphasis on how to spend your retirement rather than how much is needed.

Pasted my reply/info from that thread:

Some great info on this thread, and some very inspirational thoughts and ideas too.

Fantastic reading the things that people actually DO with their retirement time – and I’d like to find out more, as many people think that once they stop working, that’s it: Boredom. Personally, I don’t get that, as @blokeuptheroad said, there’s an endless universe of opportunity if you think about it.

I’d like to hear more people’s thoughts and ideas about how they actually spend their time in retirement… my ideas below.

But first, for those who don’t know what their financial situation is, or how they’ll fund retirement, I recommend doing the following:

1. Start by tracking what your outgoings are today with your current lifestyle.

– Download some expense tracking software that automatically sucks in and categorises the transactions from your bank accounts, credit cards etc. Make sure you go though it regularly to ensure the categorisations are correct.

– This may sound like drudgery, but it’s actually fun, and there’s tremendous value in knowing what you’re actually spending rather than guessing.

– So far as apps go, I’ve used BankTivity and Quicken in the past, but MoneyHub is my favourite these days – simple, easy, brilliant, UK-not-US centric, and inexpensive at £10/year.

2. Do the above for at least 6 months then extrapolate it on a spreadsheet to a full year.

– Obviously, a year or more gives you much more reliable data and takes account of seasonal fluctuations such as Christmas, summer holidays, birthdays, etc.

– Doing this will give you an insight into what your actual spending is.

– Now, project out how you think your spending in each category will change in retirement. For example, in our case we reduced the amounts each year for groceries (as we won’t be feeding a family of 5), child & dependent expenses, clothing, cars (as we won’t need the 3 we currently have), car insurance, telephones & mobiles, and so on – and increased the amounts we’ll likely spend on travel/holidays, hobbies, entertainment, eating out, medical expenses, gifts, etc.

3. Get control of your Pensions

– If, like me, you don’t know what your pensions amount to (I had 9 pensions from 6 employers over 29 years), contact all your providers and get statements for retirement income and/or transfer out values.

– Consider carefully whether what your money is actually invested in (the ‘underlying’) and whether it is in the right place(s).

– In my case, once I saw it all laid out I was shocked at how poorly some of my pension pots were performing – then embarrassed/ashamed at how how many years I’d ignored doing anything about it (!).

– As to what your money should be invested in, well, there’s no one right answer for everyone. But if, like me, you’ve ignored it for some time, or if you’re not sure – then clue yourself up! Get sure. Do a bit of reading up on how to invest, what Funds are, what Index Trackers are, what Bonds are, what other investments are. If that all sounds too boring, go and see an IFA – but beware of high fees for some funds.

– Just clue yourself up and start to make better choices. *see point 5 below.

4. Project out (again, using a spreadsheet) what all your future sources of income will be p/a (State Pension, personal Pension, investment income, savings income, other sources of income if you have them), and compare it to your projected annual outgoings from Step 2. You’ll immediately see if you’re ‘good to go’ or not.

– If not, consider how you can reduce your current spending in order to save/invest more.

– The financial insight you have gained from step 2. above will be invaluable as you do this.

5. Clue Yourself Up.

– I won’t get into the debate here about the 4% rule, where to invest/what to invest in, pensions, savings, etc… there’s a bazillion books and articles out there already. But for anyone who’s interested in retiring early there are some valuable sources of info out there.

– Start by reading JL Collins’ “The Simple Path To Wealth’ (and/or read his blog), listen to the ‘MadFientist’ podcast (and other ‘FIRE’ podcasts), read ‘Mr Money Mustache’s’ blog, etc.. Just Google ‘FIRE’ and start browsing.

Now onto the more interesting stuff: ‘What to do with your time once retired’…

I’m 55 and am in the fortunate position of being financially independent. No, I didn’t inherit a fortune. No, I didn’t make millions in the City. And no, I am not a drug dealer :-). I’ve never been given a thing and have had to work hard – very hard – for everything I’ve got. Often it was too hard, missing my kids birthdays, suffering incredible stress/burnout, nearly losing a marriage.

I’ve always avoided debt as much as possible and lived within my means. That is a core principle. Ok, we had a big mortgage (and miraculously managed to pay it off early), but aside from a mortgage we’ve avoided debt completely. We’re fortunate, in that yes, we could afford nice cars and stuff if we wanted them, but I always looked at my mates driving the latest BMW or whatever and thought “They’re nuts.. that £40k car will depreciate £20k in 2 years. I’d rather buy a £5k or £10k car and drive it for 5 years then sell it for £2k”.

That kind of philosophy goes a long way – and applies to most things in life. Life is not about material possessions: the nicest house, blingest car, the latest iPhone, gadget or doo-dad, a new Sky+ box, or whatever. Life is not about ‘Stuff’. We have more material possessions today than our grandparents or ancestors ever had – yet there is no evidence that they were any less happy. Life is about friendships, love, contribution, happiness, health, etc.

So.. what are those things for you? I’d love to hear what makes people happy.

What are the things you’d do if you retire today?

And for those who are already retired/have achieved FI, what do you do with your time?

For me, these are the things that are important to me:

– Go for walks with my wife & dog in the countryside

– Drink coffee with my wife/visit Cafe’s and just talk

– Continue to be a loving, supportive Dad to my 3 kids

– Ride my bike – with friends

– Spend a season or two (probably in a CamperVan) following the Pro road cycling season: starting with Flanders/Paris Roubaix, then onto the Giro, le Tour, la Vuelta and culminating at the Giro di Lombardia (not slavishly following every stage of every tour, but coming and going as we please, to the stages/places that interest us)

– Spend a month or so in summers hiking around the Alps/Pyrenees with a knapsack on my back

– Ski more, until such time as we’re unable to

– Laugh more

– Contribute more to our local Community (my wife has run the Cubs/Scouts for the past 12 years, I’ve volunteered at camps, village fetes etc… but I want to have more of an impact. I want to make a bigger contribution).

– Do more Yoga. I love it and always feel better.

– Vitality/Health/Fitness/Mobility/Wellbeing: walk, run, yoga, cycle, maybe take up some calisthenics, reading.

Ignore.

The real question for me is how do you fill your time during a winter like this unless you have plenty of cash?

I'm intrigued as to why spending loads of cash is necessary to fill your time during a winter lockdown? Unless it's illegal/immoral travel what would you spend your money on?

Don't get me wrong, I'd happily (until Mrs Kenny found out and killed me) go onto Wiggle now and spend thousands easily. Or buy loads of other things. However none of them are really necessary to make life enjoyable.

There's a ton of stuff out there to do that costs nothing or very little, even in the depths of winter.

Just an observation, many folks in here very focused on “retirement” as in stopping working. I think work in some form is really good for most people be it paid, a business or voluntary.

Nope. No way.

Just an observation, many folks in here very focused on “retirement” as in stopping working. I think work in some form is really good for most people be it paid, a business or voluntary.

Not meaning to be offensive but that thought to me shows a total lack of imagination

First summer retired me and t'missus are going to do a long walk - several hundred miles

first winter - was supposed to be south america trekking. covid may have effed that up. Second summer - long cycle tour round europe. Several thousand miles. 2nd winter - antipodes for a road trip.

Other things planned - tour of the india sub continent to take in some big cricket matches, Highlands and islands bike tour, more walking in Europe

how do you fill your time during a winter like this

Cycling or running with friends (obvs 1 at a time ATM). Walking the dog and having the time to not stress as he stops to snack on goosegrass. Catching up with all the stuff I've not had the time or mental space to do while working - music, art, books, films. Doing more proper cooking as I've got the energy to concentrate on something with more than just one step in the recipe! Hacking away at the garden.

The best thing is being able to get as much daylight as I want in winter, not being stuck at my desk.

Not meaning to be offensive but that thought to me shows a total lack of imagination

If I understand his sentiment correctly I don’t think he’s wrong. There’s a point you can achieve where you’ve paid of the mortgage and have saved a decent amount for later life whereby instead of retiring per se you can “downsize” your job to less hours, less stress, less responsibility - whatever floats your boat - because you no longer have the financial stress/responsibility. This is a path I’m taking, working damn hard now but saving madly with a plan to be devoid of mortgage and save/invest to reduce the effort of working in 3 years - aged 53 - from now. I’ll still work and save, but not the 70hr week sales stress I’m dealing with now.

Digger, it sounds to me like you had a crap life until you get to retirement age. I saw every single bithday of my son, put him to bed every night and made him breakfast most mornings. I work, but it's in IT and i'm not sure it counts in the same way as digging roads 🙂

I'll do ok when i retire, but before then i do things like trips to Morzine, i do trackdays at Spa, Jerez, Portimao on one of my 2 motorbikes i have here...

TBH mate, i think it sounds to me like you're the one who's got it wrong, not me.

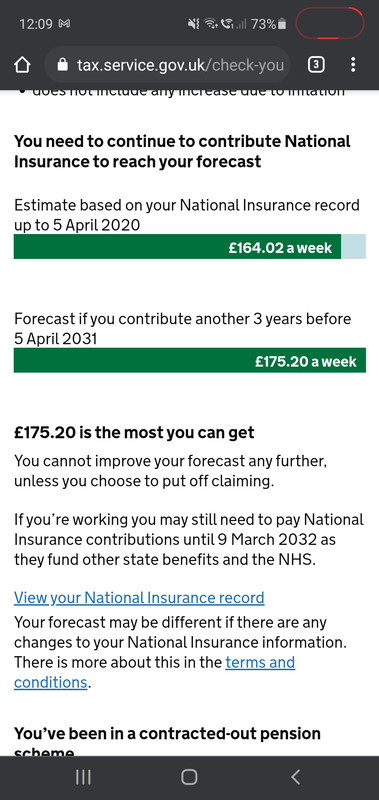

You have:

36 years of full contributions

11 years to contribute before 5 April 2031

4 years when you did not contribute enoughYour forecast is £175.20 a week.

£175.20 is the most you can get

You cannot improve your forecast any more.

I'm 56 BTW, left school at 16 and went to college.

I've taken a few years out from work though (as per the 4 years stated above).

Also, in one of my qualifying years', contractor, I paid £5.45 in NI contributions 🙂

I was reading back as Weeksy responded. Longer members on here will know I've enjoyed a journey away from over-materialism, but ultimately both of you are right, and inevitably this thread lends itself to people of our age and life experience.

You should understand how to save and invest to enjoy your picture of a realistic future, but you also need to enjoy life as it is today. My post above is based on living a decent standard of life (subjective of course) with the kids now, whilst also achieving our plan for retirement.

Yes, there should be a retirement plan, but once you're on that journey there's no reason any extra's can't be used for Weeksy's trip to Morzine. for example. And if you can't find something to enjoy it with, just save it.

All of this comes back to “wants v needs.

Let’s be honest, the “Needs” are covered by the state pension plus a bit. Any extra spend/earlier retirement is generally a Want.

any NHS people on here bought the additional pension benefits (APB) , the reply from SPPA was less than helpful or clear.

I had almost 30yrs contracted out by employer, but paid enough through secondary employment and self employment that all the haters hated 😊

Well this thread has given me some homework - I've been through my spending over the last year and have done a review of savings and pension pots etc and the net is that when you add them all up I have 30-40 years of typical spend before I factor in the state pension (starting in 12 years). For clarity, I don't spend much so that's not as big a number as it might sound.

So now I know I'm working because I choose to, or perhaps because I'm actually a bit scared about what to do if I stopped (I've been unemployed before and my mental health suffered badly). My job is interesting and rewarding, but not as interesting or rewarding as things like riding my bike on a summer's day - but there's a lot of time left over. On the flip side I've already dropped to 4 days a week because I had stuff to do and no time to do it but I don't think the last year has helped me value that. Fwiw I don't think there's much scope to drop my working days any further at the moment.

Also I'm not sure MrsP is giving it quite as much thought as me, so if I did quit I'd likely be flying solo for a bit.

More thinking needed I reckon, need to delve into what's actually keeping me at work...

any NHS people on here bought the additional pension benefits (APB) , the reply from SPPA was less than helpful or clear.

depends on what scheme you are in. I am in the 96 section and could not buy additional years

On the flip side I’ve already dropped to 4 days a week because I had stuff to do and no time to do it but I don’t think the last year has helped me value that. Fwiw I don’t think there’s much scope to drop my working days any further at the moment.

I've dropped to 4 day week and still don't have enough time. Tempted to try 3 day week soon...

The real question for me is how do you fill your time during a winter like this unless you have plenty of cash?

I think a lot comes down to where you chose to live at this stage in your life. We have deliberately chosen to move to somewhere where it is easier to create a more sustainable lifestyle (grow your own / local produce etc). The community also provides ample opportunity for volunteering and maybe part-time work. I also set-up a small online business 3 years ago with a view that it could be operated from anywhere that has the potential to generate a small income and can also be extended to offer some B2B sales locally. At today's rates, we can get by on £18k/year - which is about half of what my pensions will yield. I've already got a camper van, 7 bikes and 2 dogs - apart from a small sailing boat, there's probably little else I can think I would like right now.

@tjagain wife in 95 scheme and a special case, (in more ways than one) midwife can retire at 55 instead of 60

Special Class membership allows you to apply for your full 1995 section pension entitlement from the age of 55 rather than the normal pension age for the 1995 section which is 60.

as she is only P/T looking to buy APB to boost pension but SPPA less than helpful with reply

OK, time to get back to work you lot, you're wrecking the economy!

haha this is my thread. I had forgotten about it. Too late. Ive submitted my notice to retire in march 2023 🙂

Too late.

Selfish bastard! Inflation is all your fault!

Interesting to re-read this thread. I am nw semi-retired (since April 21), living on savings until I can access my pensions in a couple of years, plus a bit of part time work. Even with the squeeze on living costs affecting my budget things are good - it is surprising how expensive working can be, and if you have more time things are actually much cheaper.

In terms of filling my time, between a PhD and elderly parents there is no lack of things to be doing, but I do find it hard ot get up before about 0800 these days (used to be in the office 1hr15mins drive away by 0730 when working....)

haha this is my thread. I had forgotten about it. Too late. Ive submitted my notice to retire in march 2023

Lucky bugger, I'm (36) currently trying to figure out if it's possible to ever get off the working to pay the mortgage treadmill.

Feels like the whole system is rigged against retirement. Saving for a deposit is a PITA because of student loan repayments, saving for a retirement is a PITA because of mortgage repayments, and by the time the mortgage is paid off it's too late to figure out how to put all that money you suddenly have spare into a pension to accrue any meaningful compound interest.

Lucky bugger, I’m (36)

I reckon quite a few financially stable retirees would would happily swap to be 36 again 🙂

Its still worth chucking money into the pension pot. With the tax advantage, compound interest and rising stock market long term you will do OK. I had very little in mine at 36.

Make sure you have something left in the pot when you eventually pop your clogs. You can't rely on the afterlife being completely free.

Thisisnotaspoon it feels like and and I'm sure that's by design to keep people working, consuming and most importantly paying taxes.

If I could speak to my younger self advice would of been buy a house sooner, stop buying crap you don't need and salary sacrifice earlier into pension to prevent the gov getting it.

I left it late and didn't get myself into gear till at least 40.

I'm one of those selfish bastards that are "crashing the economy" at the moment by being retired at 57.

No actually if most employers didn't crush the very soul out of experienced staff with utterly pointless stuff we would have probably kept working as we used to enjoy it and always took real pride in our jobs.

Due to big changes in the personal side of my life 😀 I’m setting up as self employed in the new financial year or I’ll get slightly bored (lot of tax to avoid for now) and I’m going to be the pickiest sod going as to what I take on. But so far all concerned are beating my door down 😮

Like I said it will be to suit me and fit in around my “new life”

davey - you have no dependants but do you have a will? If you don't, the state will benefit when you die.

If you do, have you checked to see what happens to your pension as, given your circumstances, it's likely that when you die it dies with you.

It might be sensible to get a transfer value and explore the options; likely you will need an IFA and acceot you will incur a mid-high 4 figure fee.

I dont have 400k in savings. But I left my job at 59. A good decision for me.

Frank - no and I keep meaning to get around to it. All to animal charities when I pull my finger out and get it sorted.

But I don't like to talk about my charity work.

£6k a year? I somehow manage to spend £6k a month - hence I don't have £400k stashed away.

51 and wondering if I'll ever retire 🙁

I don't have £500k but I thought f--k it and packed in work about 9 months ago (age 61).

I'm "surviving" on an small £15k defined benefit pension from an old civil service job I did many years ago - that just about covers my month-to-month expenses.

But I do also have some investments and savings as well. I'm burning through the savings (did some DIY on house, just back from a decent holiday and I've just ordered a new bike!) but haven't needed to touch the investments yet. And I'll have state pensions kicking in eventually.

Initially, I was very cautious about budgeting but I'm coming to realize that I should have enough "fixed income" to easily cover a reasonable lifestyle (though I'm not the extravagant type)

Mrs Vlad is still working, the mortgage is paid off and we don't have any kids to consider so my circumstances aren't exactly common...

Good to hear it’s working well. It’s interesting to consider lifestyle changes that can make it happen too.

We made the decision last September after the consultant told Kevin if he wanted to carry on riding then he needed to do it now as his shoulder and arm would deteriate to the point he couldn't

We both finished at the end of March and had a three week trip to ride in Italy at the end of April.

3 weeks back in the UK to get the van MOTed and service along with a hospital appointment for me.

We are now 3 days into a five week riding trip.

Today was 30 miles and 3000m of descent.

Going to enjoy it whilst we can. So glad we took the plunge

An old work pension, I had forgotten about, tracked me down from 3 properties ago the other day. It is a defined benefit which is forecast to be £4k p.a. when I am 65 years. Might pay for a holiday or half my marina fees in the future. They wouldn't give me a transfer value as the market is too volatile. This was before Trump started WW3. Suspect the other pots I do know about are going to get hammered tomorrow!

those that look the leap in the last few years with pots ranging up to 500k or so, how is it working out ? For you, for your partner if there is one ?

Not directly answering your question, but still sort of relevant.

Wanted to take voluntary redundancy in spring with a ca £60k package but the wife wasn't in favour, so I didn't. Really wondering how I'm going to get through the next three years.

Just so tricky to work out how much money it needs.

those that look the leap in the last few years with pots ranging up to 500k or so, how is it working out ? For you, for your partner if there is one ?

Not directly answering your question, but still sort of relevant.

Wanted to take voluntary redundancy in spring with a ca £60k package but the wife wasn't in favour, so I didn't. Really wondering how I'm going to get through the next three years.

Just so tricky to work out how much money it needs.

Don't know your lifestyle or income, but I'd have ripped their hands of for a £60k payoff. First £30k is usually tax free, so even on 40% tax onnthe rest, that's still something like £48k in hand. For most folks thats heading towards 2 years worth of net wages. You could have filled any gap with a supermarket job.

Worst thing my dad did was not take a decent pay off at Leyland DAF. 2 years later the Co went into administration (of course Thatcher let it go bust without any intervention) and he just got statutory minimum instead from the Gov. Basically he worked the last 2 years for nothing.

small £15k defined benefit pension

How large a pot do you suppose it would cost to buy that kind of annuity - £300k ? Not that small really.

Try something around the £400,000 to £500,000 mark...

Don't know your lifestyle or income, but I'd have ripped their hands of for a £60k payoff. First £30k is usually tax free, so even on 40% tax onnthe rest, that's still something like £48k in hand.

In this scenario you should put the amount above £30k into a SIPP so would pay zero tax at that point.

The big eye opener for me is the combination of 25% tax free lump sum, no NI and staying in the 20% tax bracket makes your money go a lot further.

The big eye opener for me is how little tax I'm now paying which makes your money go a lot further

Ive been trying to work out scenarios around that. Using a drawdown and with the first 25% being tax free, so hypothetically say that chunk was 150k, I’m assuming that could be taken at a rate of say £3000 a month for 5 years without paying any tax at all ?

I'd have ripped their hands of for a £60k payoff. First £30k is usually tax free, so even on 40% tax onnthe rest, that's still something like £48k in hand. For most folks thats heading towards 2 years worth of net wages.

Yep, agreed on all points. Basically I'm working the next year for nothing at all.

I think basically the missus wasn't keen on working and me not. Which I can understand. But then she has career goals etc and doesn't want to retire yet. I very much do want to retire and get on with my life before I am too old.

I'd have ripped their hands of for a £60k payoff. First £30k is usually tax free, so even on 40% tax onnthe rest, that's still something like £48k in hand. For most folks thats heading towards 2 years worth of net wages.

Yep, agreed on all points. Basically I'm working the next year for nothing at all.

I think basically the missus wasn't keen on working and me not. Which I can understand. But then she has career goals etc and doesn't want to retire yet. I very much do want to retire and get on with my life before I am too old.

Interesting thread

I was forced in to 'retirement' in January when I was made redundant aged 51.

What I have found in the following months is that for me

1. I am not ready to retire

2. Having time on your hands is great, but everyone else is out working + I have now bike nearly all the trails within a 3 hr drive of where I live that have been on my bucket list

3. You can do all DIY jobs etc that need doing at home, but the easy/cheap ones get done fairly quickly, then it gets expensive, then you think will you live here long enough to justify it.

4. Its fairly cheap to get out and about in your local area doing stuff, but overnight stays these days are not cheap.

5. Mrs FD is still working, son still at school so limits what I can do ie going away etc

6. Utopian part time work does not exist

7. Utopian voluntary work does not exist (given constraints of 5 above)

So luckliy Ive found a fixed term contract, and actually what we have learnt from this is that I may be able to work for 6 ish months a year, and still have a redundancy payment in the bank.

I think it has made us both realise that we could / should both try and retire no later than early 60's

@FunkyDunc - I definitely wasn't ready aged 50. Financially, I'd have been fine but mentally, I still needed something - and my wife was still working too. That meant I ended up doing part time work, but something I really enjoyed and completely different from my previous career.

At age 60 I was definitely "ready".