![]() You don't need to be an 'investor' to invest in Singletrack: 6 days left: 95% of target - Find out more

You don't need to be an 'investor' to invest in Singletrack: 6 days left: 95% of target - Find out more

I'm not suggesting that this is good advice but I saw a video this morning, if I understood it right, there is an option to buy an annuity at say 60 that would run to 68 and your state pension, then they give you back a big lump to choose your next option.

Like I say, might not be the best idea but its an option I wasn't aware of.

I don't agree with the time in the markets thing. Some market timing things have helped our finances cosiderably as I'll elaborate below. I'm cautious and only buy into things I understand which has meant I've missed some "opportunities" such as bitcoin/crypto because I still don't have any faith in "owning" a bit of code. As noted by others above it does feel a bit Spring 2000 again, I think there's a good chance of being able to buy back in at these levels sometime in the future so I'm not bothered by being light at present. I might be wrong, I'm not worried. We're small players - a soon to retire teacher and stay at home dad with the modest wealth we have generated by a business in the 90s.

Madame sold a house in early 89 just before a crash (people around us thought we were daft to sell but it avoided a nasty negative equity situation). We bought into another country in the market lows that followed.

In Spring 2000 we converted a share portfolio into the house I'm sitting in against the advice of several financial "experts" who thought I should take a mortgage and keep the shares. It would have taken nearly 20 years for that share portfolio to recover and some of it never would have.

I've bought in dips in the market fairly regularly but without conviction over the last 23 years and have just sold a chunk to buy a property. Buying the dips has resulted in better gains than if I'd dumped a lot in at a random point. I'd rather be in (useful) property than ETFs right now.

If I'd just just sat in the markets I'd be poorer and I'd have had more to worry about due to an aggregate higher exposure. Currently even if the markets drop 50% I can just shrug because my exposure is so low.

In terms of the other debates on this thread I haven't joined in with I'm something of a fan of annuities. OK they're a bad deal if you die quickly but you aren't going to spend time worrying about the loss, you'll be dead. My parents made the choice of taking a bigger lump sum and a smaller annuity which by the time they reached 90 they could see hadn't been the best choice.

No idea what went wrong on that last post, at bottom of page 11, format all over the place..🙄

Maybe some of the expert market timers we have on this thread can tell us whether Friday's dip was a blip or the start of something bigger? Or is it one of those where the wisdom only comes out in hindsight?

For people who worry they are exposed to the Mag 7 there are plenty of alternative ETFs to switch into instead of bailing out completely. For example, XWCS is a World Consumer Staples ETF is seen as a defensive play and has 58% of the fund spread across these 10 holdings - Walmart, Costco, P&G, Coke, Philip Morris, Nestle, Pepsi, Unilever, BAT and L'Oreal. Energy ETFs are another option.

I don't agree with the time in the markets thing.

Not sure its Warren Buffets entire investment strategy. But it seems to be panning out for him OK. Hes got lots of those throw away quotes attributed to him and taken as a whole the do add up to a fairly sensible, slightly conservative approach to investing. Re your good fortune, great that those timings worked in your favour but riding the roller coaster does come with risk. My dad lost big on an endowment .mortgage, which 12 months before were the golden ticket.

Maybe some of the expert market timers we have on this thread can tell us whether Friday's dip was a blip or the start of something bigger? Or is it one of those where the wisdom only comes out in hindsight?

This is like the 4th time Trump has done this now, people have short memories... it's just another market manipulation for/by the ultra rich...its always on a friday as markets close over the weekend.

I'm supprised the markets reacted as much as they did to be honest.

...an unknown, one day old account shorted bitcoin 30mins before trumps anouncement, and pocketed a tidy $88 million. That's just one transaction.

Good timing? don't make me laugh.

The game is rigged, all we can hope to do as retail investors/traders is ride the waves and keep our heads above the water line... the real money, the uninmaginable volume of money that can fix entire countries, even global healthcare, social issues, etc, is being made at the top table, and they don't share.

So yes it's just a blip, ride it out and don't sell. If you do anything, buy.

Or is it one of those where the wisdom only comes out in hindsight?

Well obviously yes. You never know if it's the right choice the day you make it, but at least it's a choice rather than burying your head in the sand and hoping which is what what the "time in the markets" approach amounts to.

You don't have to time perfectly, you can start to lighten up as you see value falling away and go back in progressively as prices look more attractive after market falls. Bookmark this page and we can see if I'm right about being able to buy back in cheaper at some point in the future. If STW survives that long. Because things never stay still and each time the markets take a dip some of the real economy drowns as people draw in the purse strings.

Maybe some of the expert market timers we have on this thread can tell us whether Friday's dip was a blip or the start of something bigger?

The mumblings about an upcoming market correction have been around for at least a week. I decided to take my profit from my ss isa which probably takes a week to process. So hopefully it doesn't drop too far before it lands in my account.

I'll continue to invest in my SS ISA as the dip continues.

No chance of retiring until another 180 pay days have occurred. 🤔😭

There's regularly a dip on Fridays. As the budget approaches, there's almost certain to be drop to some degree. I've sold stuff high hoping to avoid a bit of a fall and buy into passive funds when they are cheaper. This isn't a recommendation, obviously.

Or is it one of those where the wisdom only comes out in hindsight?

Well obviously yes. You never know if it's the right choice the day you make it, but at least it's a choice rather than burying your head in the sand and hoping which is what what the "time in the markets" approach amounts to.

You don't have to time perfectly, you can start to lighten up as you see value falling away and go back in progressively as prices look more attractive after market falls. Bookmark this page and we can see if I'm right about being able to buy back in cheaper at some point in the future. If STW survives that long. Because things never stay still and each time the markets take a dip some of the real economy drowns as people draw in the purse strings.

I don't think it's burying your head in the sand, it's about your approach to risk. If long term market returns are good enough to achieve your goals then taking a risk on market timing is unnecessary.

I'm sure you'll be able to buy back at lower prices given current sky high valuations. But the question is how much of the bull run have you missed by being out of the market?

At the end of the day leveraged property has smashed everything else in terms of returns in this country over the last 30 years, so anyone who was fortunate enough to benefit from that has done well. Pure luck rather than judgement though.

I follow stock markets but I wouldn’t want to make a prediction as to their future direction. I’m of the “time in the market” school of thought but there does seem to be a greater than normal number of usually sane commentators muttering about the high level of shares. As I noted earlier, some of the deal making in the AI sector is enough to raise your eyebrows, but then again, I’m not really involved so I would think that. Every severe correction has a different build up and root cause although many bubbles have stories which look eerily similar - good idea makes some money for pioneers which in turn attracts more money and investors which develops into geared up speculation on things which are tenuously connected to the original idea.

For those who think they can time markets....the 1987 Crash was one of the most severe sharp corrections in history and yet even today you’ll not find an agreed cause of why it fell when it did other than “markets had had a good run and things felt a little frothy”. The extent of the fall was exacerbated by some portfolio structures in place at the time (in a similar way to the Truss crash - that correction was logical but the extent of it was magnified by certain things in place in portfolios). Because there was no stand out identifiable risk factor at large in 1987 it was pretty much an unforeseen event and a lot of money was lost in short order. And yet, despite the severity of the fall and the amount of money lost, if you look at a graph of the long term history of the stock market this correction is nothing more than a minor ripple.

Having the foresight to sell ahead of a big correction or the nerves to invest cash after a big fall is harder than it sounds but I wouldn’t blame anyone who has an identifiable need for money in the next six months or has made more money than they “should” have done in recent months for choosing to harvest some cash now "just in case”.

But the question is how much of the bull run have you missed by being out of the market?

None so far, I lightened up at the March highs just before the Trump tarifs spooked the markets, and knowing I'd need a lot of it within seven months. The stuff I sold is at almost exactly the same level this morning. If anything I feel over invested at present, I'll have a look today. I could have bought back in in anticipation of a rally after the initial spook but that's with hindsight, as it was I was happy to have reduced exposure and still feel the same way. The markets have long periods in which I feel confident they aren't stupidly over valued and unlikely to crash, why stay in for the short periods I think risk is high. No question mark, that's just the way I do it.

I agree with Blackhat about having the nerve to go in hard again after a fall. I've found that harder than selling before a fall. I tend to go back in progressively so don't get the full benefit of the bounce.

None so far, I lightened up at the March highs just before the Trump tarifs spooked the markets, and knowing I'd need a lot of it within seven months. The stuff I sold is at almost exactly the same level this morning.

You must have had some slightly poor stocks then if that's the case. Almost all mine are a shit ton higher than they were in march. As mentioned previously I'm up close to 30% on gold but even the stuff I left in is up about 15 or 20% from pre trump.

Yup, some of the funds I've kept have done better but not 15-20%, some have stagnated, one has lost a bit: generally the less ethical sectorially and geographically the better they've done. 🙁 The under performance has been small cap France and Europe.

I'm about as far from knowledgeable as you can be, but got spooked a couple of weeks ago and moved 50% of my Vanguard ISA into cash. Will probably shift a fair portion of it into a cash ISA in due course. Rest of it and pensions will stay as they are and hope for the best. The ISA has done remarkably well but it's not going to last forever

I'm about as far from knowledgeable as you can be, but got spooked a couple of weeks ago and moved 50% of my Vanguard ISA into cash. Will probably shift a fair portion of it into a cash ISA in due course. Rest of it and pensions will stay as they are and hope for the best. The ISA has done remarkably well but it's not going to last forever

So did you leave the cash in the ISA, or withdraw it?

Fixed Term ISAs look interesting for those who are risk averse. With £400K, you can get £25k per year for 25 yrs and still get £100K back at the end (so value of £725k ish). Obviously that's not index linked, but your state pension will be once it kicks in.

@boxelder I've left it as cash within the ISA for the time being, will look at either transferring some or all into a cash ISA or dribbling it back into investments when I feel a bit more confident

No need for the administrative hassle of moving ISA wrappers - especially as you may well reverse your decision at some point and the admin delay may mean that point passes before you can act - buy a short dated gilt instead or find a money market fund.

So this morning it looks like Friday was blip:

And we're now left with reporting season, borrowing against invoices, random trade tarifs, endebted governments, AI bubble, war, cheap energy, gravity defying p/E ratios, low interest rates and bond yields (Europe) and a host of other factors to weigh up. From a simple supply and demand point of view there are still plenty of people rich enough to have a surplus to invest and chase value with, and drive the markets. The problem being that squirreling money away is bad for the economy and bad for the companies they are squirreling money away in (mainly a japanese and European issue).

Good luck with your guessing, I made my decisions in March and sleep well. 🙂

But the question is how much of the bull run have you missed by being out of the market?

None so far, I lightened up at the March highs just before the Trump tarifs spooked the markets, and knowing I'd need a lot of it within seven months. The stuff I sold is at almost exactly the same level this morning.

Sorry if it seems like I'm trying to pick on you, that's not my intention. It's essentially a debate about active Vs passive investing strategies where you prefer active and I prefer passive (albeit constantly having to resist the temptation to have an active dabble).

In this particular example, if you'd have adopted a passive approach and invested in a global index fund in March then you'd be about 15% up by now. So it seems your active decisions in respect of both stock selection and timing have lowered your returns on this occasion. Although if the market drops back below the March level again, which it may well do, you might still feel vindicated.

I read Edukator’s post as implying he realised some investments because he knew he had some cash needs in the immediate future and his commentary was on what remained. Less an active vs passive strategy, more a bird in the hand vs two in the bush approach, and totally understandable.

At the end of the day leveraged property has smashed everything else in terms of returns in this country over the last 30 years, so anyone who was fortunate enough to benefit from that has done well. Pure luck rather than judgement though.

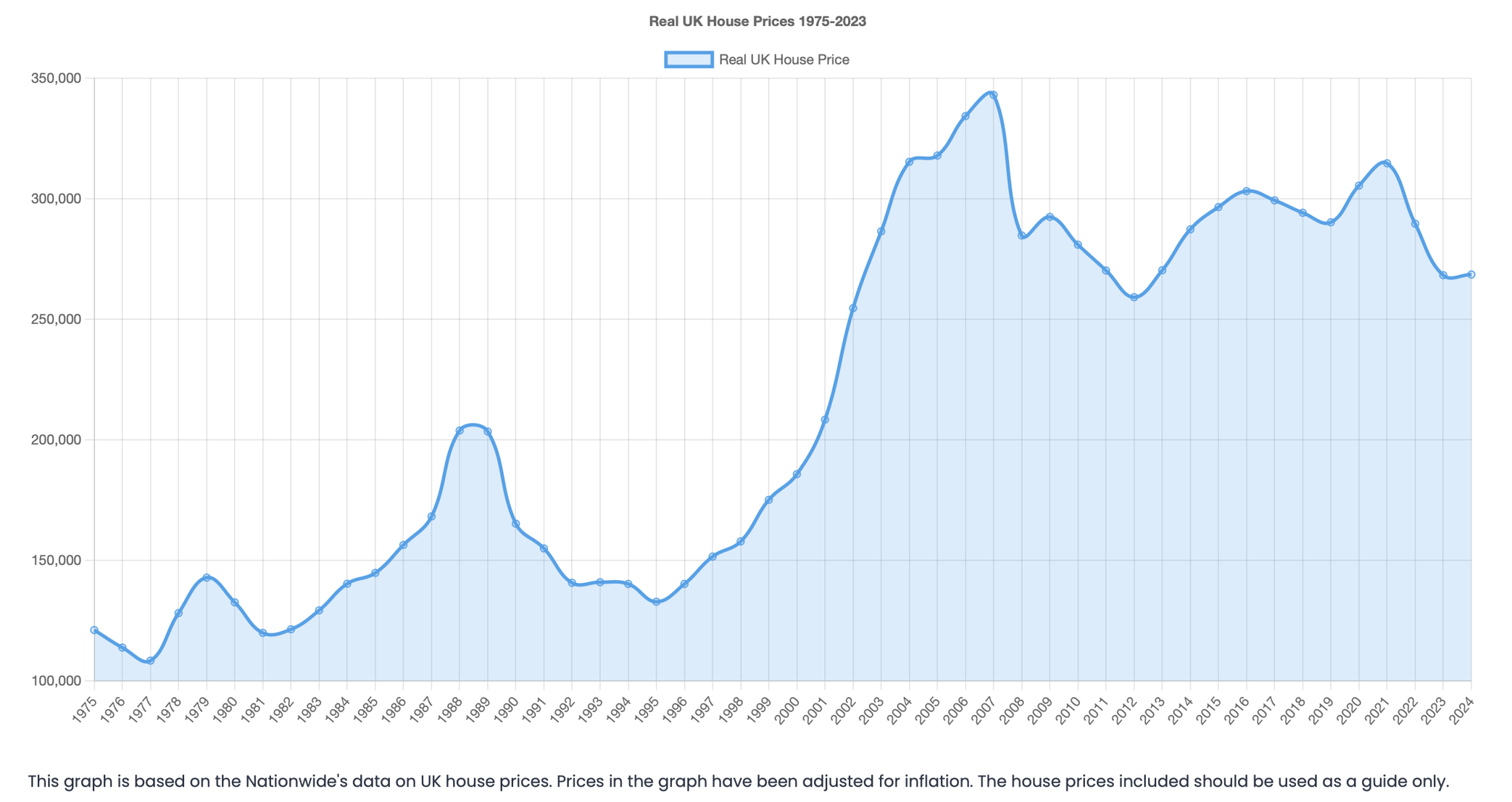

I posted this the other day. If you bought property in the 90's you've done really well. Post 2000? not so much - we're only now where we were in 2003 in real terms.

Thing is I don't want to be in a Global Index fund, Roli Case. The stocks in those indexes are some of the most overvalued in my view. The boom in index linking is part of what I see as a bubble and I don't want to be a part of that at this point in time. Even if I'd invested in index funds I don't see how I'd have got 15% since March. No gain since March is pretty good for someone investing in Euros.

The rise of Euro against the dollar would have eliminated any gains compared to US indexes. The Euro is up 12% since March

Euro pound is up about 8% and the FTSE about the same

Eurostox 50 is where I sold

The CAC has gone nowhere

I could have made money in Asia even though the Euro is strong. I sold out of Asia about ten years back when I finally saw a reasonable profit after years of ups and downs. Asian ETFs are a lottery IME.

So from my Euro investor point of view any gains since March have been from lucky/wise choices rather than following indexes. And in pound terms the portfolio I've kept is nicely up, even the one I said had "underperformed" is positive in pounds..

Dow futures looked promising earlier but as we get closer to the open not so.

There are all sorts of thematic ETFs..

Global minus USA... 'VXUS' for example, or global developing marks, etc etc.

There's an ETF for all occasions!

Global ETFs and s&p500 ETFs are the most popular at the moment as that's where most returns are made currently..

And you can split your money between a couple to accomplish what sort of weighting you want.

For example I'm about 60% in 'all world' and about 40% in developed Europe (large and medium cap companies).

I was about 7% up overall since April which is pretty good going, but I'm only about 5% up after Friday's shenanigans. It'll recover over the next week I'm sure.

My basic philosophy is if I make 7% over 12 months tax free I'm happy, any more is a bonus.

"A couple", I've lost count, somewhere around 12. 🙂

"A couple", I've lost count, somewhere around 12. 🙂

Lol. You might want to look at consolidation if you've got 12?!

Seems a bit excessive! But if it works for you it works.

My basic philosophy is if I make 7% over 12 months tax free I'm happy, any more is a bonus.

So, I'm 5 years off my teachers DB pension and want to retire. For £54K of my SIPP, I can get £12000/year for 5 years from a fixed term annuity. That's the same as a guaranteed annual growth of around 4.5% if I left that £54K at the mercy of markets and used flexi draw down. I'd still have the rest of my SIPP and ISA invested, but this could ride out 5 years of instability quite nicely.

If I left the £54k and got 7% per year growth, but drew £12000/year, I'd have ~£1700 left at the end - but will the next 5 years give 7%....??? I guess the chances are very good, as annuities are sold by insurance firms who crunch the numbers and calculate the odds. I don't need more from it though and it would be guaranteed. 🤔

<off to the classifieds in search of a crystal ball or ravens entrails....>

My basic philosophy is if I make 7% over 12 months tax free I'm happy, any more is a bonus.

So, I'm 5 years off my teachers DB pension and want to retire. For £54K of my SIPP, I can get £12000/year for 5 years from a fixed term annuity. That's the same as a guaranteed annual growth of around 4.5% if I left that £54K at the mercy of markets and used flexi draw down. I'd still have the rest of my SIPP and ISA invested, but this could ride out 5 years of instability quite nicely.

If I left the £54k and got 7% per year growth, but drew £12000/year, I'd have ~£1700 left at the end - but will the next 5 years give 7%....??? I guess the chances are very good, as annuities are sold by insurance firms who crunch the numbers and calculate the odds. I don't need more from it though and it would be guaranteed. 🤔

<off to the classifieds in search of a crystal ball or ravens entrails....>

Depends entirely where you are at in life and what you want, there's no 'one size fits all' strategy. Generally people (and pensions) 'de-risk' as they get older to avoid impact from market crashes, so they might transition more to bonds than equities, etc.

But I'm only mid 40's so I'm going hard on equities at the moment, and I can afford to ride the waves of a stock market crash without panic selling...

..If I were 2 years from pension age though, I'd have a much more conservative attitude.

I didn't have time to edit my post, when I say 'going hard on equities' I mean big ETFs, not individual stock picking/stock trading, I'm quite conservative in my strategy, 'buy the whole market' if you have time to ride any dips out, rather than spinning the wheel and buying individual stocks/shares.

The returns are less exciting, but the risk is a lot lower, too.

boxelder. The 4.5% guaranteed on the annunity is what treasuries around 5 years are yielding so the insurance company offering that annuity is taking very little risk. No risk to you, reasonable return - that's sounds pretty good for money you know you are going to spend over the next five years. 5 years is too short to ride out ups and downs on money you know you're going to need. Imagine you'd taken the risky option in Summer 2000 and see where that would have left you. If you think about it it's better than 4.5% because they have less and less of your money to invest as they give it you back. More like 7%

High risk strategies are for money you don't need in the short term and may never need at all.

For those thinking the market in AI is overpriced and is going to crash/slump/dip/adjust..... Well, you're not the only ones.

https://youtube.com/shorts/efPNRNtbOdY?si=wXAjthiLCdibQomx

Channel4 News podcast is out there on this topic. Worth a listen.

I'm counting the days till November when I can cash out my employee share options. If I can do that before the crash then I think I'll be reasonably covered.

If I don't then......

Hmmmmmm. I have instructed a matured cash ISA to be transferred to Vanguard with a view to opening a S&S ISA all allocated to the VWRP ETF.

The request hasn't been executed yet so think I might just dump the cash into another cash ISA..

I'm counting the days till November when I can cash out my employee share options. If I can do that before the crash then I think I'll be reasonably covered.

My employer is the largest gas consumer and B2B supplier in Germany. 90% of our supplies came from Gazprom before the Ukraine war, and for a year or so we had to make up all the lost volumes at market spot prices when the supplies stopped overnight.

Shares lost 98% and really haven't recovered because basically we got taken over by the German government and there's none to trade on the market.

It's a good job I'm not relying on those as part of my retirement planning. 😭

I think that the AI engineers and CEOs don't understand probability and exponential functions very well. To my mind, AI is almost certainly going to burn out and not show most of the improvements that it is purported to.

However it doesn't matter what I think, it's what the rest of the market thinks that matters. In order to time the market, I both need to be correct, and at the right time. Being correct at the wrong time is just another form of being wrong in business and finance IMO.

Hmmmmmm. I have instructed a matured cash ISA to be transferred to Vanguard with a view to opening a S&S ISA all allocated to the VWRP ETF.

The request hasn't been executed yet so think I might just dump the cash into another cash ISA..

Vanguard platform charges platform fees, on top of the fund management fee. If you want to buy a vanguard ETF, you're best buying it within a stocks and shares ISA on a fee-free platform such as T212 or invest engine.

My basic philosophy is if I make 7% over 12 months tax free I'm happy, any more is a bonus.

If I left the £54k and got 7% per year growth, but drew £12000/year, I'd have ~£1700 left at the end - but will the next 5 years give 7%....??? I guess the chances are very good, as annuities are sold by insurance firms who crunch the numbers and calculate the odds. I don't need more from it though and it would be guaranteed. 🤔

Not that it will make much difference to the decision on this amount but wouldn't it be more like £4k left assuming you draw down monthly rather than yearly?

Your average investment for calculating returns in Yr 1 is £48k, not £42k, and so on.

Not read all of this but are you a couple with no mortgage? How much do you give yourself each week?

^^ not sure which post that is asking about. There was a lot of chat quite a few pages ago on the magic number for a couple on their own without a mortgage. I recall the average was around 3-4.5k per month, after tax, to cover all life costs.

If you think about it it's better than 4.5% because they have less and less of your money to invest as they give it you back. More like 7%

The quick calculation I did was subtracting the drawdown each year, so fairly sure it matches 4.5%. I'd always seen annuities as too conservative/playing too safe, but a short term one could safely see me to DB pension starting, so I now know I can afford to become an idle ne'erdowell retire. It's still a chunky decision though, with my wife not wanting to retire and employers needing to fill the (small) gap I'd leave

.

My basic philosophy is if I make 7% over 12 months tax free I'm happy, any more is a bonus.

If I left the £54k and got 7% per year growth, but drew £12000/year, I'd have ~£1700 left at the end - but will the next 5 years give 7%....??? I guess the chances are very good, as annuities are sold by insurance firms who crunch the numbers and calculate the odds. I don't need more from it though and it would be guaranteed. 🤔

Not that it will make much difference to the decision on this amount but wouldn't it be more like £4k left assuming you draw down monthly rather than yearly?

Your average investment for calculating returns in Yr 1 is £48k, not £42k, and so on.

Correct (probably). I was doing some crude sums to get the approximate annuity AER and then applied the same to the 7% growth i.e. subtract £12k, multiply by 0.07 etc.

I always thought all this shizz was dull, but once you realise it can stop you having to turn out for work.........

Why worry about your employers filling the gap you leave? It’s not your problem, and if it is a problem for them you might find they offer you a sweeter end to working life such as flexi/part time work or more money until they do find a replacement.

They're friends and it's already PT/Flexi. It's not really an issue if I give notice.

I always thought all this shizz was dull, but once you realise it can stop you having to turn out for work.........

I do also think it’s easy to overthink it all, I’ve certainly found that to an extent.

Why worry about your employers filling the gap you leave?

"The Indispensable Man" by Saxon White Kessinger

Sometime when you’re feeling important;

Sometime when your ego ‘s in bloom;

Sometime when you take it for granted,

You’re the best qualified in the room:

Sometime when you feel that your going,

Would leave an unfillable hole,

Just follow these simple instructions,

And see how they humble your soul.

Take a bucket and fill it with water,

Put your hand in it up to the wrist,

Pull it out and the hole that’s remaining,

Is a measure of how much you’ll be missed.

You can splash all you wish when you enter,

You may stir up the water galore,

But stop, and you’ll find that in no time,

It looks quite the same as before.

The moral of this quaint example,

Is to do just the best that you can,

Be proud of yourself but remember,

There’s no indispensable man.

^^ that’s great, not seen it before.